The banking industry in 2023 has been disrupted by a series of unexpected events, throwing the global financial markets into disarray. Within a single week in March, three small to mid-sized U.S. banks, including Silvergate Bank, Signature Bank, and Silicon Valley Bank, failed. The collapse of these banks led to a sharp decline in global bank stock prices and triggered an immediate response by regulators to prevent a potential global contagion.

The failure of these banks can be attributed to their significant exposure to cryptocurrency and mismanagement of their Treasury bond portfolio. As market interest rates rose, the value of the bonds they held decreased significantly, causing depositor concerns about the bank’s liquidity. This situation was further complicated by the fact that these banks primarily served technology companies and wealthy individuals who held large deposits that exceeded the Federal Deposit Insurance Corporation (FDIC) insured limit of $250,000.

In response to this crisis, U.S. federal bank regulators announced extraordinary measures to ensure that all deposits at the failed banks would be honored. The Federal Reserve established a Bank Term Funding Program (BTFP) to offer loans of up to one year to eligible depository institutions pledging qualifying assets as collateral.

Global industry regulators also intervened to provide extraordinary liquidity to prevent the situation from affecting more banks. Notably, in Switzerland, UBS acquired Credit Suisse in a government-brokered deal to halt the banking crisis. This prevented the systemically important financial institution from collapsing, which would have caused further crisis within the banking system.

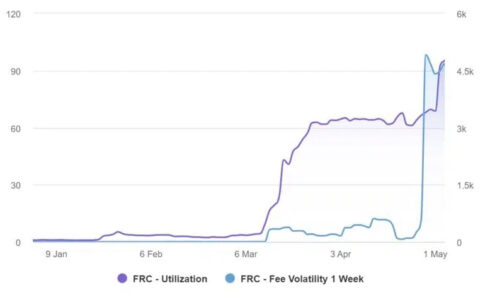

The crisis further instigated a bank run at San Francisco-based First Republic Bank, which had a large portion of uninsured deposits exceeding the FDIC limit. Despite a $30 billion capital infusion from a group of major banks, the bank continued to destabilize, and eventually, it was sold to JPMorgan Chase.

An analysis of the events leading to the crisis reveals a few key factors. Firstly, many U.S. banks had invested their reserves in U.S. Treasury securities, which had been paying low interest rates for several years. As the Federal Reserve began raising interest rates in 2022, bond prices declined, decreasing the market value of bank capital reserves, and causing some banks to incur unrealized losses. Secondly, several banks gained market exposure to cryptocurrency and cryptocurrency-related firms, which turned out to be a risky move given the turbulence in the cryptocurrency market.

In addition, the collapse of Silicon Valley Bank sent shockwaves through the financial markets and eroded confidence in other banks. This resulted in a significant drop in bank stock prices. In a flight-to-safety response, there was a plunge in government bond yields, which also affected the market.

To mitigate the risk of a bank collapse, it is crucial to maintain a robust capital cushion to absorb losses. Banks such as JP Morgan, Bank of America, Citigroup, Goldman Sachs, Wells Fargo, Bank of New York Mellon, and Morgan Stanley, also known as Global Systemically Important Banks (G-SIBs), have high capital requirements and are subjected to additional regulatory scrutiny, which has helped them to stay resilient during the crisis.

Another lesson from the 2023 banking crisis is the importance of managing the size of securities portfolios relative to deposits. Banks should avoid excessive exposure to volatile assets like cryptocurrencies and ensure that they maintain a balanced portfolio that can withstand fluctuations in the market. Silicon Valley Bank’s inordinate size of securities portfolios relative to deposits led to massive losses in its bond portfolios when yields rose.

The banking crisis also highlighted the importance of FDIC insurance. Banks serving wealthy clients with average account sizes significantly larger than the FDIC insurance limit are at higher risk during a banking crisis. For example, only 3% of Silicon Valley Bank’s deposits qualified for FDIC insurance, and the bank’s average account size was $1,251,000 compared to $177,000 at the average regional bank. In the event of a bank failure, uninsured deposits above the FDIC limit can be lost, which can trigger a bank run as large account holders have a strong incentive to withdraw their money.

Despite the crisis, the U.S. banking system maintains a multi-decade high capital level. While some banks have shown weaknesses due to rising yields and fluctuations in the economy, the sector does not appear to be at a high risk of systemic failure or collapse. Nevertheless, continued turmoil within the banking system could weigh on the overall market and the economic outlook3.

In the wake of the banking crisis, the Federal Reserve is likely to continue raising interest rates, albeit at a slower pace, to combat inflation. However, the rate hikes may be smaller than previously expected due to the ongoing crisis and its impact on the financial system4.

The 2023 banking crisis serves as a reminder of the importance of maintaining robust capital buffers, managing risk exposure, and ensuring adequate deposit insurance. It also underscores the role of regulatory oversight and swift intervention in preventing a full-scale banking crisis. However, the situation is still evolving, and investors are advised to closely monitor developments and understand the potential risks when investing in the financial sector5.

As we navigate through these uncertain times, it is crucial to learn from this crisis and continually refine our strategies to ensure the stability of the banking industry. With careful planning, risk management, and vigilance, we can work towards a more resilient and robust banking system for the future.

In conclusion, the 2023 banking crisis offers a stark reminder of the interconnectedness of global financial systems and the potential for rapid contagion when weaknesses are exposed. While regulators and central banks were quick to respond and prevent a broader systemic failure, the crisis has exposed vulnerabilities in our banking systems that must be addressed.

The issues that led to the crisis, such as exposure to volatile markets, over-reliance on uninsured deposits, and risky investment strategies, underscore the importance of prudent risk management and regulatory oversight in maintaining the stability of financial institutions. It is crucial that lessons are learned from this crisis to prevent similar situations in the future.

Moreover, the crisis serves as a reminder to investors of the importance of understanding what they own when investing in the financial sector. While the overall U.S. banking system remains robust and is not at a high risk of systemic failure or collapse, particular pressure may continue on banks perceived to be weaker by the markets.

Finally, the crisis highlights the essential role of central banks in managing economic stability and maintaining confidence in the financial system during times of stress. The measured response of the Federal Reserve and other global central banks during this crisis has been key in averting a broader financial meltdown.

As we move forward, the focus must be on strengthening our banking systems, improving regulatory oversight, and promoting prudent risk management practices. Only then can we navigate through these uncertain times and build a more resilient and robust banking industry for the future.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/lessons-from-the-2023-banking-crisis-analysis-impacts-and-strategies-for-resilience.html