Introduction

Inflation is one of the most persistent threats to long-term financial health. Even moderate inflation gradually erodes the purchasing power of your money, which can wreak havoc on a retirement plan if left unaddressed. As a financial advisor and investing expert, I often recommend a diversified approach that not only grows your portfolio but also preserves its value against inflation.

Among the strategies to inflation-proof your portfolio, the mega backdoor Roth stands out as a powerful but often overlooked tool for high-income earners. In this post, we’ll explore seven effective ways to protect your investments from inflation, including how the mega backdoor Roth strategy can boost your tax-advantaged retirement savings and help your portfolio stay resilient over time.

1. Invest in Stocks for Long-Term Growth

Equities are historically one of the most effective hedges against inflation. While stock markets are inherently volatile, over the long term, they tend to outpace inflation and generate real returns.

- Why it works: Companies can increase prices during inflationary periods, preserving profit margins and shareholder value.

- What to do: Consider broad-based index funds (like the S&P 500) or dividend-paying stocks for a balance of growth and income. For added resilience, tilt your portfolio toward sectors that benefit from inflation, such as energy, utilities, or consumer staples.

2. Utilize Treasury Inflation-Protected Securities (TIPS)

TIPS are government bonds designed specifically to guard against inflation. Their principal value adjusts with the Consumer Price Index (CPI), ensuring that both your principal and interest payments keep pace with inflation.

- Why it works: TIPS offer built-in inflation protection while maintaining low risk.

- What to do: Allocate a portion of your bond holdings to TIPS, particularly if you’re nearing retirement and want to reduce exposure to inflation risk.

3. Incorporate Real Assets Like Commodities and Real Estate

Real assets tend to appreciate in value during inflationary periods. This category includes tangible investments such as commodities, real estate, and infrastructure.

- Why it works: Real assets often have intrinsic value and can rise in price along with general inflation trends.

- What to do: Invest in REITs (Real Estate Investment Trusts), commodity ETFs (covering gold, oil, etc.), or direct property investments for diversification and inflation protection.

4. Consider the Mega Backdoor Roth Strategy

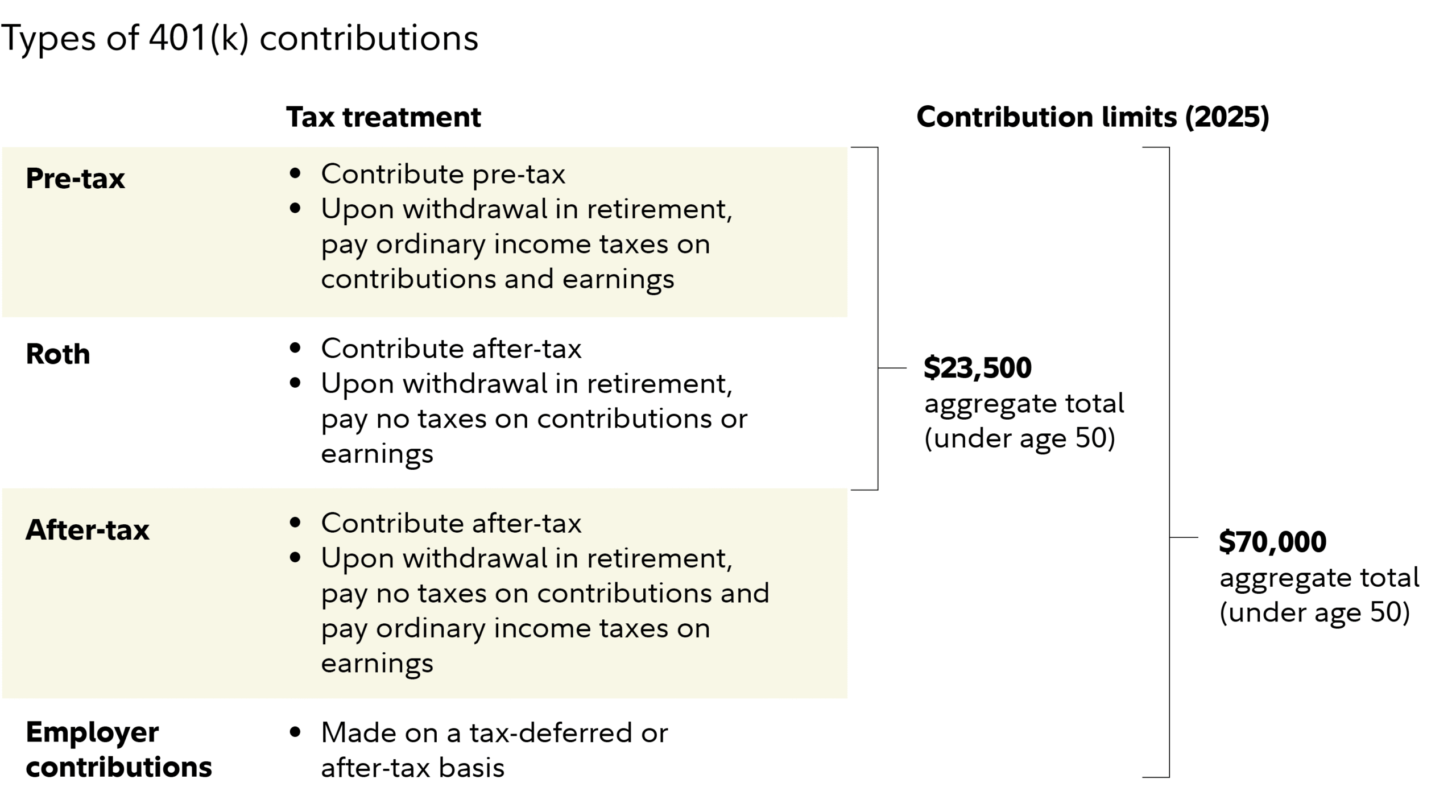

One of the most powerful tax-advantaged strategies available to high-income earners is the mega backdoor Roth. It allows individuals to convert after-tax 401(k) contributions into a Roth IRA or Roth 401(k), enabling significantly more tax-free growth.

How it Works:

- Step 1: Maximize after-tax contributions to your 401(k), beyond the standard $23,500 limit ($31,000 for those aged 50–59, and $34,750 for ages 60–63).

- Step 2: Convert those contributions into a Roth account—either via in-plan conversion or a rollover into a Roth IRA.

This can allow total annual contributions up to $70,000–$81,250, depending on age and employer contributions.

Why It Helps Inflation-Proof Your Portfolio:

- Tax-free growth: Roth accounts are not taxed on future earnings or qualified withdrawals, so your money grows tax-free—ideal for combatting inflation’s erosion over time.

- No RMDs: Roth IRAs are not subject to required minimum distributions, allowing you to let your money grow longer.

- Flexibility: Once in a Roth, your funds can be invested in equities, TIPS, or real assets—boosting your inflation defense across the board.

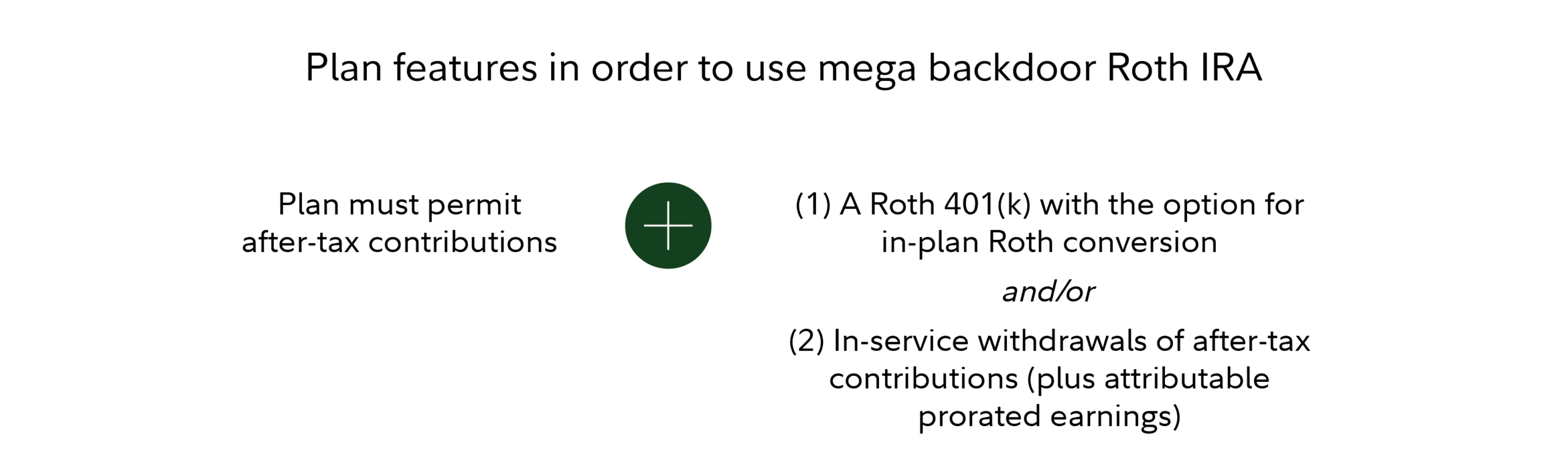

- Important: Not all employer plans support after-tax contributions or in-service rollovers. Review your plan documents or speak to HR to confirm your eligibility.

5. Maintain a Globally Diversified Portfolio

Inflation doesn’t move in lockstep across countries. By diversifying internationally, you reduce dependence on a single economy’s inflation trends and open your portfolio to opportunities in emerging and developed markets alike.

- Why it works: Currency fluctuations and regional inflation patterns create opportunities for risk management and return enhancement.

- What to do: Allocate a portion of your equity and fixed-income investments to international markets, including developed economies like Europe and Japan, and emerging markets like India and Brazil.

6. Use Tax-Advantaged Accounts Strategically

Beyond the mega backdoor Roth, other tax-advantaged accounts like traditional IRAs, Roth IRAs, HSAs (Health Savings Accounts), and 529 plans help shield your gains from taxes—which is particularly valuable in inflationary periods when nominal income increases.

- Why it works: Keeping more of your returns by avoiding taxation helps preserve purchasing power.

- What to do: Max out annual contributions to traditional and Roth IRAs, take advantage of catch-up contributions if you’re 50+, and consider HSAs for health-related retirement costs.

7. Stay Flexible with a Dynamic Withdrawal Strategy

In retirement, how you withdraw money matters just as much as how you saved it. A dynamic withdrawal strategy can help you adapt to inflation and market volatility by adjusting your spending based on market conditions.

- Why it works: Inflation can spike unexpectedly, so static withdrawal plans may fall short.

- What to do: Consider the “Guardrails Strategy” or “Dynamic Spending Rules” that adjust withdrawals based on portfolio performance and inflation levels.

You can also segment your portfolio into buckets:

- Short-term (cash, T-bills)

- Medium-term (bonds, TIPS)

- Long-term (stocks, Roth accounts)

This helps ensure you’re not forced to sell growth assets in a downturn or high-inflation period.

Final Thoughts: Inflation is a Silent Threat—But You Can Outsmart It

Inflation quietly erodes your wealth over time—but it’s not unstoppable. By taking proactive steps to build an inflation-resilient portfolio, you can preserve and grow your purchasing power for decades to come.

The mega backdoor Roth strategy is a particularly potent tool for high earners who want to turbocharge their tax-free savings and defend against future tax increases and inflation. While it requires careful setup and employer plan compatibility, the long-term benefits can be substantial.

Remember: Not all strategies are appropriate for every investor. Consult with a financial advisor or tax professional to ensure these tools align with your goals, risk tolerance, and retirement timeline.

By combining equity exposure, tax-advantaged growth, real asset allocation, and dynamic withdrawal planning, you can build a portfolio that doesn’t just survive inflation—but thrives despite it.

About the Author

As a licensed financial advisor and investing expert, I help individuals and families create resilient, tax-smart portfolios designed to meet both short-term needs and long-term goals. I specialize in retirement planning, wealth preservation, and advanced Roth strategies like the mega backdoor Roth. If you’re ready to inflation-proof your financial future, let’s connect.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/7-proven-strategies-to-inflation-proof-your-investment-portfolio-including-the-mega-backdoor-roth.html