Watching the stock market swing up and down can be nerve-wracking—even for seasoned investors. The headlines may fuel anxiety, and the temptation to “do something” can be strong. But reacting emotionally to a market downturn is rarely a recipe for long-term financial success.

Instead, a volatile or declining market can be an opportunity to reinforce your financial foundation, realign your portfolio with your goals, and even create potential tax advantages. Whether you’re a new investor or a long-time saver, there are strategic steps you can take to help protect your wealth and set yourself up for future growth.

Here are five essential money moves to consider during a down market:

1. Shore Up Your Emergency Fund

When the economy shows signs of strain, your first line of financial defense is your emergency fund. This cash reserve helps cover essential expenses like housing, groceries, healthcare, and transportation in case of income disruption—such as job loss, reduced hours, or unexpected expenses.

As a general guideline, aim to save 3 to 6 months’ worth of essential living expenses. If you’re just starting, setting aside $1,000 as an initial cushion is a good milestone. From there, work toward your longer-term savings goal.

If you’re the sole income earner in your household or in a field susceptible to layoffs, consider aiming for the higher end of that range—or even more. A robust emergency fund buys you peace of mind and helps avoid pulling money from investments during market lows, which can lock in losses and derail your long-term strategy.

2. Make Investing Automatic with Dollar-Cost Averaging

In volatile markets, it’s easy to let emotions take over. Fear and uncertainty can lead to hesitation or even pulling out of the market entirely—often at the worst possible time. That’s why automating your investments through dollar-cost averaging (DCA) is so powerful.

With DCA, you invest the same dollar amount on a regular schedule—monthly, for example—regardless of whether the market is up or down. When prices fall, your fixed investment buys more shares; when prices rise, you buy fewer. Over time, this smooths out your cost basis and removes the need to “time the market.”

Let’s say you invest $250 every month into a mutual fund. If the market dips, that $250 goes further—allowing you to accumulate more shares at lower prices. And when the market rebounds (as it historically does), those extra shares can amplify your gains.

This simple yet effective strategy encourages discipline, reduces market timing risk, and helps you stay invested—key principles for long-term wealth building.

3. Review and Rebalance Your Portfolio

Market gains and losses can cause your investment allocations to drift away from your original targets. For instance, if stocks have performed well in recent years, your portfolio may now carry more equity exposure than you intended, potentially increasing your risk beyond your comfort level.

Conversely, after a downturn, certain asset classes—like bonds or international stocks—may now be underweighted.

Rebalancing involves bringing your portfolio back in line with your desired asset allocation. This means selling overweight positions and buying underweight ones, effectively forcing you to “buy low and sell high.” It’s a disciplined approach that helps manage risk, maintain diversification, and ensure your investment mix still matches your goals, time horizon, and risk tolerance.

Consider reviewing your portfolio annually or after major market moves. And if you work with a financial advisor or use a robo-advisor, they may already rebalance for you automatically.

4. Explore Tax-Loss Harvesting Opportunities

A down market can open the door to potential tax advantages through a strategy known as tax-loss harvesting. If you sell investments at a loss, those losses can be used to offset capital gains elsewhere in your portfolio, potentially reducing your tax bill.

Even if you don’t have capital gains, up to $3,000 in net losses can be used to reduce your ordinary income annually. Any additional losses can be carried forward to future years.

For example, say you own a tech stock purchased at $10,000, now worth $7,000. Selling it locks in a $3,000 loss, which could offset other gains or income on your tax return.

However, this strategy requires careful planning:

- Avoid wash sales: The IRS disallows a tax loss if you buy the same or “substantially identical” investment within 30 days before or after the sale.

- Don’t compromise long-term goals for a short-term tax benefit.

- Consult a tax professional, especially if you’re managing your investments yourself.

Some investment managers already handle tax-loss harvesting automatically, so check with your provider before acting.

5. Consider a Roth Conversion While Asset Values Are Low

A declining market may present a unique opportunity for tax-savvy investors: the Roth conversion. This involves transferring assets from a traditional IRA or 401(k) to a Roth IRA, paying taxes now in exchange for tax-free growth and withdrawals in the future.

When your portfolio is down, the value of the assets you’re converting is lower—so the tax bill for the conversion is also lower. In effect, you’re getting a discount on the future tax-free status of your investments.

Benefits of a Roth IRA include:

- Tax-free growth and tax-free withdrawals in retirement (if qualified)

- No required minimum distributions (RMDs), unlike traditional IRAs

- Estate planning advantages, since Roth IRAs can pass on tax-free to heirs

However, keep in mind:

- The converted amount is treated as ordinary income in the year of conversion, so coordinate with a tax advisor to avoid bumping into a higher tax bracket.

- Ensure you have cash on hand to pay the taxes, rather than withdrawing from the account to cover the bill.

If you’ve been considering a Roth conversion, a bear market may be an opportune time to act.

Final Thoughts: Stay the Course and Think Long Term

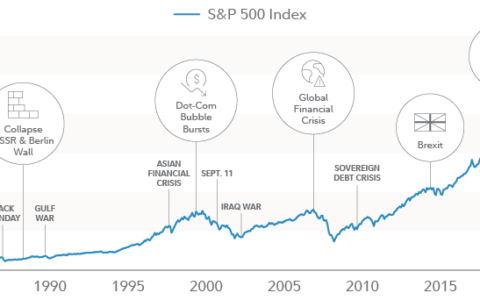

Market downturns are an inevitable part of investing. While they can be unsettling, they also offer opportunities—for reflection, adjustment, and strategic action. The key is to avoid knee-jerk reactions, and instead focus on what you can control: building your cash reserves, sticking with your investment plan, managing taxes, and aligning your portfolio with your financial goals.

History shows that markets recover—and those who remain patient and proactive are often better positioned when the tide turns.

So rather than panic in the face of volatility, use this time to strengthen your financial foundation. Your future self will thank you.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/5-smart-money-moves-to-make-in-a-down-market-2.html