Tax season can be a stressful time of year for many individuals and business owners. Understanding how to maximize your tax savings can help ease some of the burden and can help you keep more of your hard earned money. Here are 20 tips to help you make the most of your tax savings.

Introduction

Taxes can be a burden for many individuals and businesses, but there are ways to save money when filing taxes. Whether it’s through deductions, credits, or other strategies, taking the time to understand your options can help you save a significant amount of money. Here are 20 tips to help you maximize your tax savings.

Understand the Basics of Tax Savings

The first step to saving money on your taxes is to understand the basics of tax savings. This includes understanding the tax brackets and the deductions, credits, and exemptions for which you may be eligible. Knowing the basics will help you determine the best strategies for saving money and can help you make the most of your tax savings.

Take Advantage of Tax Deductions

Tax deductions can reduce your taxable income and can result in a lower tax bill. Common deductions include those for mortgage interest, medical expenses, charitable contributions, and state and local taxes. It’s important to understand the deductions for which you may be eligible and to take advantage of them when filing your taxes.

Claim All Tax Credits for Which You Qualify

Tax credits are even more valuable than deductions because they directly reduce the amount of taxes you owe. Some common tax credits include the Earned Income Tax Credit, the Child Tax Credit, and the American Opportunity Tax Credit. It’s important to understand the tax credits for which you may be eligible and to claim them when filing your taxes.

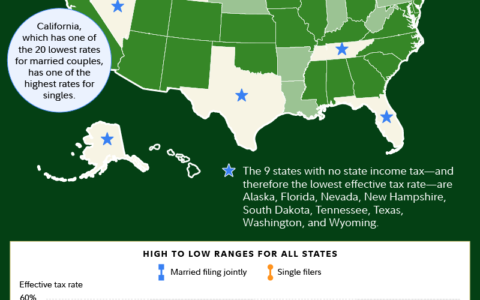

Consider Your Filing Status

Your filing status can have a significant impact on your taxes. Different filing statuses can result in different tax brackets and can impact the deductions and credits for which you may be eligible. Understanding the different filing statuses and how they may affect your taxes can help you save money when filing your taxes.

Estimate Your Tax Liability

Before filing your taxes, it’s important to estimate your tax liability. This will give you an idea of how much you may owe in taxes and can help you plan for any payments you may need to make. It can also help you determine if you need to make additional contributions or adjustments to reduce your tax liability.

Plan Ahead for Retirement

Planning ahead for retirement is an important part of saving money on taxes. Making contributions to a traditional IRA or 401(k) can help you save for retirement and can reduce your taxable income. It’s important to understand the different retirement accounts and to make contributions to them throughout the year.

Make Tax Advantaged Investments

Making tax advantaged investments can help you save money on taxes. Tax advantaged investments include those in municipal bonds, real estate investment trusts, and certain other investments. It’s important to understand the tax advantages of these investments and to make contributions to them in order to maximize your savings.

Utilize Tax Deferred Accounts

Tax deferred accounts can help you save money on taxes by allowing you to defer taxes on the money you contribute to them. Common tax deferred accounts include 401(k)s and IRAs. It’s important to understand how these accounts work and to make contributions to them in order to maximize your savings.

Take Advantage of Tax Free Income Streams

Certain income streams are exempt from taxes, allowing you to keep more of your hard earned money. Common tax free income streams include Social Security and certain types of investments such as municipal bonds and annuities. It’s important to understand the different tax free income streams and to take advantage of them when filing your taxes.

Utilize Professional Tax Advice

Working with a tax professional can help you maximize your tax savings. A tax professional can help you understand your options, identify potential deductions and credits, and ensure that you’re taking full advantage of all available tax savings.

Conclusion

Taxes can be a burden, but understanding how to maximize your tax savings can help you keep more of your hard earned money. Taking the time to understand the basics of tax savings and to take advantage of deductions, credits, and other strategies can help you save a significant amount of money.

Top 20 Tips To Help You Maximize Your Tax Savings

- Take advantage of tax deductions and credits: There are many deductions and credits available to individuals and businesses that can help reduce your tax bill. Some examples include deductions for charitable donations, student loan interest, and business expenses.

- Contribute to a retirement account: Contributions to a traditional IRA or 401(k) can be tax-deductible, which can lower your taxable income.

- Keep track of your expenses: Make sure to keep accurate records of your expenses throughout the year, as they can be used to claim deductions or credits on your tax return.

- Stay organized: Keep all of your tax-related documents in a safe place so that you can easily find them when you need them.

- Take advantage of the standard deduction: The standard deduction is a set amount that can be taken off of your taxable income without itemizing your deductions.

- Consider itemizing: If your deductions exceed the standard deduction, it may be more beneficial to itemize your deductions.

- Take advantage of the earned income tax credit: This credit is available to low to moderate income individuals and families and can help reduce your tax bill.

- Take advantage of the child tax credit: The child tax credit can help reduce your tax bill if you have dependents under the age of 17.

- Take advantage of the saver’s credit: The saver’s credit is available to individuals who make contributions to a retirement account and can help reduce your tax bill.

- Consider a health savings account (HSA): Contributions to an HSA can be tax-deductible and the money in the account can be used to pay for qualified medical expenses.

- Take advantage of the home office deduction: If you have a home office and use it exclusively for business purposes, you may be able to claim a home office deduction.

- Take advantage of the state and local tax (SALT) deduction: You can deduct state and local income, sales, and property taxes up to a certain limit.

- Take advantage of the mortgage interest deduction: Interest paid on a mortgage for a primary residence can be deductible.

- Take advantage of the charitable donation deduction: Donations made to qualified charitable organizations can be deducted from your taxable income.

- Take advantage of the education tax credits: There are two education tax credits available: the American Opportunity Tax Credit and the Lifetime Learning Credit.

- Consider a flexible spending account (FSA): Contributions to an FSA can be tax-deductible and the money can be used to pay for qualified medical or dependent care expenses.

- Take advantage of the energy-efficient home improvement credit: If you make energy-efficient improvements to your home, you may be eligible for a tax credit.

- Take advantage of the adoption credit: If you adopt a child, you may be eligible for a tax credit.

- Take advantage of the small business health care credit: Small businesses with fewer than 25 full-time equivalent employees may be eligible for a tax credit for providing health care coverage to their employees.

- Consult with a tax professional: If you have any questions or concerns about your taxes, it’s always a good idea to consult with a tax professional who can help you maximize your savings.

No matter what stage you’re at in your tax preparation process, taking the time to understand your options and to take advantage of tax savings can help you keep more of your hard earned money. Don’t miss out on available savings. Take the time to understand how to maximize your tax savings and make the most of your tax return.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/tax-saving.html