Central banks around the world made quite a splash last week, with the Federal Reserve and the European Central Bank meeting expectations with a 25-basis point policy rate hike. Yet, the real surprise came from the East with the Bank of Japan (BOJ) presenting an unexpected shift in the Yield Curve Control (YCC) policy.

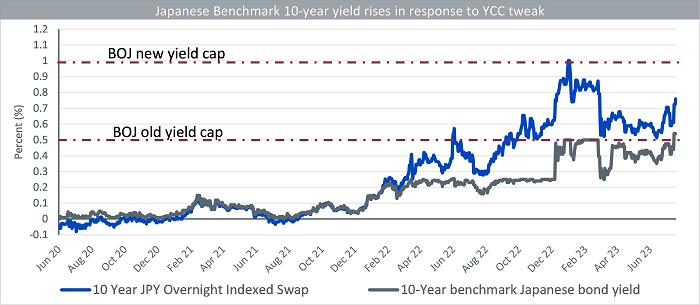

This unexpected move from the BOJ marks a commencement of their withdrawal from the YCC, as they now permit a deviation above the long-term rate cap of 0.5%, and have upped the rate for the 10-year Japanese Government Bond (JGB) fixed-rate purchase operations to 1%. In essence, the BOJ is effectively broadening their YCC band, acknowledging the policy’s outlived utility over the past seven years. This is quite intriguing, especially considering that just a week prior, Governor Kazuo Ueda emphasized the BOJ’s patience with the current monetary framework.

The sudden move, which caught 82% of economists surveyed by Bloomberg by surprise, is indicative of the central bank’s determination to control market speculation, similar to the last YCC policy adjustment made in December 2022. In doing so, they mitigate the potential adverse effects of market speculation on the JGB curve, reducing the need for heightened interventions.

That said, it is vital to underline that past performance cannot serve as a guarantee for future results and that any investments could decrease in value.

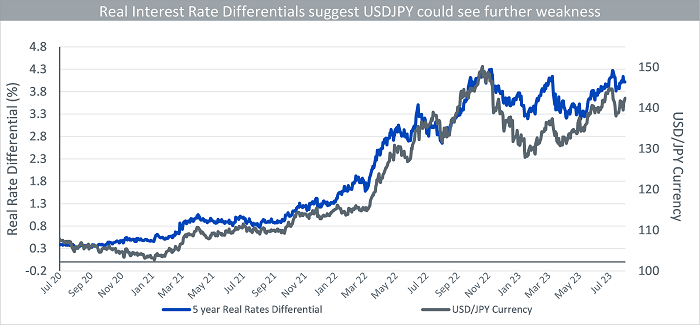

The real question is: will the revamped YCC policy, now armed with added flexibility and capable of more nimble responses, succeed in achieving the BOJ’s goal of sustainable and stable attainment of the 2% inflation target? The path to this goal remains uncertain as longer-dated JGB yields are expected to experience upward pressure until it becomes evident that Japanese inflation and wage pressure are subsiding.

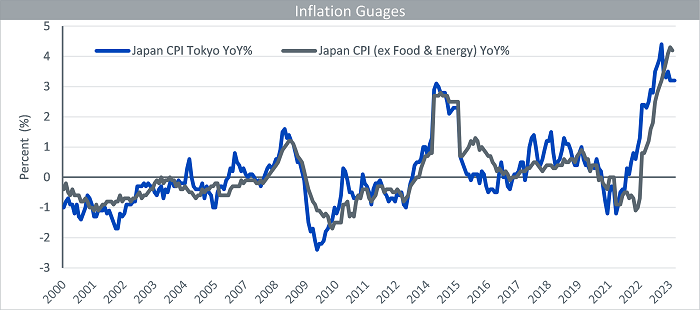

Japan has been grappling with deflationary headwinds for decades. However, we are witnessing some winds of change as firms’ wage- and price-setting behavior and inflation expectations begin to trend upwards. In fact, this spring saw some firms announcing significant wage hikes in response to a tightening labor market and rising inflation, marking a shift from the protracted trend of stagnant wages. Nonetheless, despite an overall 2.9% increase in wages in May, real wages continued to decline by 0.9%, indicating that more needs to be done to truly overcome deflation.

Another cause for concern is Japan’s headline inflation rate which stayed at 3.2% YoY in July for three consecutive months. While core inflation, excluding fresh food and energy, surged to 4.2%, the highest level since April 1982. Although headline inflation is expected to slow down due to falling global commodity prices and base effects, the core inflation rate is expected to remain high due to structural changes in the labor market.

Amidst these developments, the BOJ maintained a dovish stance with below-target inflation forecasts. It lowered its forecast for FY2024 to 1.9% and kept its FY2025 projection at 1.6%, implicitly justifying continued easing from the BOJ. Governor Ueda noted at a press conference that the 2% price stability target seems distant considering the inflation outlook for FY2024 and FY2025. This dovish narrative combined with the new YCC regime sends a clear message: the BOJ plans to continue its easing policy through an increase in the monetary base via fixed operations.

The BOJ’s surprise decision elicited an immediate reaction in the markets with a sharp rise in Japanese bond yields and an initial fall in yen value. In a surprising twist, two days post the meeting, the BOJ announced an unscheduled bond-purchase operation to curb the rise in yields, underscoring the BOJ’s ability to intervene at any time. This opaqueness could trigger more volatility across risk assets.

As we move forward into the remainder of 2023, it is clear that with the BOJ positioning the YCC as a tool to sustain its current accommodative policy, Japan’s monetary environment is expected to remain relatively loose. This is likely to result in a volatile trading range for the yen.

Remember, historical performance does not guarantee future results and investments may decrease in value. As investors and observers, it’s crucial to stay informed and adapt to these policy shifts, understanding that central banks, like the BOJ, are striving to balance economic recovery with long-term stability. It’s not just about navigating the currents but also weathering the oncoming storms. The BOJ’s policy shifts may appear subtle, but their ripples could have profound impacts on the broader economic landscape.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/balancing-act-bank-of-japans-slow-dance-with-yield-curve-control-policy.html