When it comes to taxes, you might be most worried about the big mistakes—the ones that could land you in trouble with the IRS. But for most of us, the pitfalls to avoid fall into 2 categories: simple human errors and missed opportunities to reduce what you owe in taxes. In both cases, a little extra time and some help from a tax professional can pay off in terms of your time, your money, and your peace of mind.

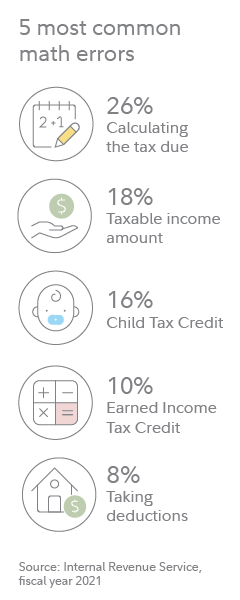

The IRS says the biggest problems with tax returns are usually simple miscalculations, followed by problems with complicated credits like the Child Tax Credit, the Earned Income Tax Credit or various deductions and credits. People also have trouble marking down the right filing status. Some get their Social Security number or bank account numbers wrong. Others forget to sign their returns.

The IRS says the biggest problems with tax returns are usually simple miscalculations, followed by problems with complicated credits like the Child Tax Credit, the Earned Income Tax Credit or various deductions and credits. People also have trouble marking down the right filing status. Some get their Social Security number or bank account numbers wrong. Others forget to sign their returns.

Most of these kinds of missteps will cost you little more than a few extra heartbeats when you get a stern letter from the IRS. The agency sent out 9.4 million “math-error” notices through April 7, 2022, according to the National Taxpayer Advocate. The largest number of such errors for fiscal year 2021 appear to have been related to the Recovery Rebate Credit and Child Tax Credit.

The more costly missteps have typically tended to involve forgetting to report investment income or missing opportunities to reduce your taxes and keep more of what you earn. Here are some common pitfalls to avoid.

1. Missing investment income

Your salary, bonuses, and other earned income get reported to the IRS on several different forms, depending on whether you are a full-time employee or self-employed. So does your investment income. Any earnings from capital gains or dividends of more than $10 will generate a 1099 tax form that you will get from your investment firm, and if you don’t claim the right amount, you could get a notice from the IRS and owe fees and penalties.

“I see those notices with moderate frequency,” says Christopher Williams, a principal at the accounting firm EY. “People sometimes have multiple accounts and it’s not uncommon for them to forget 1 or 2. But the IRS will pick it up and generate a notice.”

Another mistake Williams often sees is with people who think that if they have reinvested all their dividends and interest they won’t owe taxes. But that’s not the case. You won’t incur capital gains taxes until you sell, but any distributions are taxable in the year they were paid—even if you did not receive them directly.

2. Selling too soon

There’s a lot of useful information on your 1099 forms and account statements that can help you avoid paying more taxes on your investments than you need to. One useful piece of information is the holding period of each investment in your portfolio. Your holding period matters to the IRS because how long you’ve owned an investment before you sell it determines the applicable tax rate. If you sell an investment that you’ve owned for a year or less, this is considered a short-term capital gain and is taxed as ordinary income. If you’re in the 22% tax bracket, for instance, that’s 7% more than the 15% you may pay in capital gains tax if you held it for more than a year.

And regardless of whether your gains are short or long term, if you are a high earner making more than $200,000 per year for a single filer, and $250,000 if you are married filing jointly, then you may also be subject to the 3.8% Medicare net investment income surtax on top of your capital gains.

3. Poor recordkeeping

The amount of gain or loss you report on the sale of an investment is generally based on the sale price minus your cost basis, which is how much it cost you to acquire the investment. One watchout: The IRS requires financial institutions to report adjusted cost basis for covered securities. Taxpayers are also required to report the details of their transactions on IRS Form 1040, Schedule D and/or Form 8949.

4. Forgetting losses

Your 1099 forms will sum up your short- and long-term losses and net them up against each other. If you have net gains, you’ll owe tax on them. Williams says that many people do not realize that if you have net losses, you can use them to offset up to $3,000 of ordinary income if you’re a single filer ($1,500 if you’re married and filing separately), and carry forward any excess losses to future years.

5. Waiting too long to strategize

Your year-end tax form, by necessity, is available after December 31 of that tax year. If you’ve got a lot of realized gains, check in on them now to offset them with any realized losses, a process called tax-loss harvesting. To be most efficient, you want to constantly monitor and adjust as necessary your investment strategy. If you haven’t been doing this already, you can start now or in the new year, and if this sounds like a lot to manage, you can consult a financial professional.

6. Engaging in wash sales

Are you an active investor? Then you will want to avoid this pitfall. A wash sale is when you sell an investment at a loss and then buy an investment that is substantially identical in the 30 days before or after the sale. If you’ve done this, you might see some unusual notations in your account file, and you won’t be able to claim the loss you were expecting in the current year.

At Fidelity, for instance, if you bought a stock for $50 and sold it in July for $40, but then bought it back again at $40 in August, your cost basis for the July purchase might appear in a different color adjusted as $50 (the $40 sale plus the $10 prior loss) and there might be a small “w” to note that this was a wash sale. Your loss won’t come into play until you sell what you bought in August.

Note: Wash-sale rules currently do not apply to cryptocurrencies, as they are not regulated as securities. That means you can sell coins whose value has declined, and buy them back immediately at the same price, potentially realizing the loss while still holding the asset. Pending legislation about cryptocurrency regulations may eliminate this loophole, however, so be sure to work with a tax professional to stay on top of changes.

7. Not taking advantage of tax breaks

What can missing a tax credit or deduction cost you? Lots.

A tax credit will reduce the tax you owe dollar-for-dollar. Imagine you have a 5-year-old child. Before claiming the $2,000 Child Tax Credit, your tax bill is $5,000. After the credit, you’ll only owe $3,000.* If you’ve received some of this in advance in 2021, the totals will get reconciled on your year-end tax return. This credit can be complicated, so consider consulting a tax professional.

A deduction reduces your taxable income. To calculate your tax savings, you would multiply the value of your deduction by your top tax rate. Say you are in the 24% tax bracket and you itemize your deductions instead of taking the standard deduction. If you give $1,000 to charity, that results in approximately $240 off your final tax bill. Had you not itemized, the entire $1,000 would have been taxed at 24%.

“Another way you can think about it is that the $1,000 you gave to charity only cost you $760,” says Williams.

This reduction in taxes is why there’s so much focus on making sure you haven’t missed any deductions you can legally take, and to make sure you know the deadlines for all of them. The IRS will only flag underpayments, so any missing deductions are your own responsibility.

8. Forgetting deadlines

One last key thing to remember: Most tax deductions are calculated through December 31, like mortgage interest, 401(k) contributions, and student loan interest. But some deadlines, like those for tax-deductible IRA contributions or health savings accounts and nondeductible Roth IRA contributions, can be made by the tax filing deadline for the prior year.

Bottom line

Tax mistakes happen, but the more you understand your financial situation and tax rules, the less impact they can have on your wallet. Even if you’re using tax software or hiring a professional tax preparer, at some point, somebody must manually enter all your information, so there’s always room for human error. To reduce that possibility, make sure to educate yourself on your tax liabilities and double-check your tax returns. You can also read up on other tax moves you can make to help reduce your tax liability.

Finally, consider tax time as an opportunity to review your finances and look for opportunities to reduce your taxes. Every dollar saved is a dollar you can grow for your future.

Fidelity Viewpoints from https://www.fidelity.com/

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/fidelity-8-tax-pitfalls-to-avoid.html