Former Fed economist John Roberts does an exercise on what a lower 2023 unemployment rate projection (of 4.2%, instead of 4.6%) could do to FOMC’s SEP. To keep inflation on the current projected path, the terminal rate estimate might go up to 5.6%

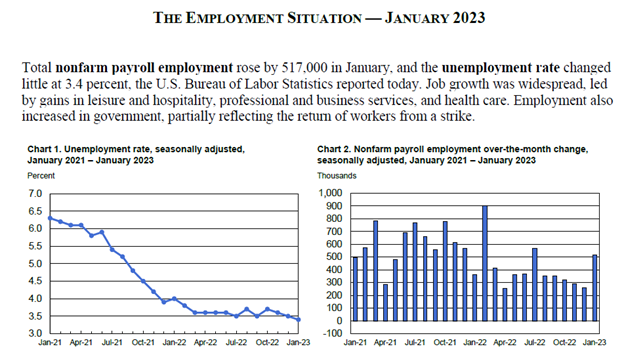

The economy in 2022 was remarkably resilient to higher interest rates and tighter financial conditions. Although residential construction fell, consumer spending continued to expand. The labor market remained strong in the second half of the year, with payrolls rising 357 thousand per month and the unemployment rate averaging 3.6 percent. And as the January labor-market report suggested, the economy’s resilience may have continued this year.

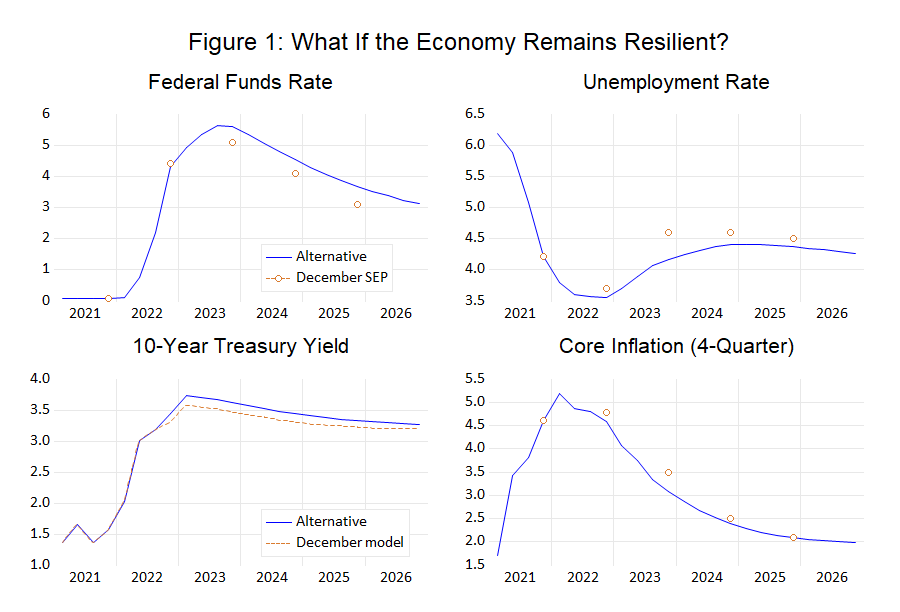

In this post, I explore the consequences of continued robust aggregate demand this year. The point of departure is a model-based analysis of the FOMC’s December economic projections (the SEP). While the main focus of the analysis is the ongoing strength in the economy, I also modify my December SEP matching exercise to take account of the incoming data on inflation, which suggest a somewhat more optimistic outlook than the FOMC assumed in December. As I discuss in more detail below, I raise the path for the federal funds rate by enough to ensure that inflation is close to the FOMC’s objective by 2025.

The results of my simulation are shown in the figure below. Continued robust growth limits the rise in the unemployment rate this year, and it ends the year at 4.2 percent, 0.4 percentage point lower than in the FOMC’s median December projection. That’s despite a steeper path for interest rates: The federal funds rate reaches 5.6 percent by the third quarter, consistent with ¼-point increases through July of this year. The funds rate stays high thereafter; it is still 1 percentage point above its longer-run level at the end of 2025. The higher expected path for the funds rate leads to higher long-term interest rates, with the ten-year Treasury yield reaching 3.7 percent this quarter. Reflecting the downward revision in response to the news about wages and prices, core PCE inflation is 3.1 percent this year, 1/2 percentage point lower than in the December SEP. By 2025, inflation is 2.1 percent, just slightly above the Fed’s 2 percent target, and in line with the December SEP.

It’s possible economy’s underlying strength could be even greater than I’ve assumed here. If it were, the unemployment rate at the end of the year would be lower while interest rates would be higher. Stronger demand in the short-run could lead to higher inflation, but it is likely that Federal Reserve policy—in the form of higher interest rates—would be aimed at ensuring that inflation is close to target by 2025.

The next section provides technical details.

Details

- For inflation, I first take on board the data on core PCE inflation for the fourth quarter of last year. As well, I undo the additional inflation pessimism of the FOMC’s December projections, reverting to an inflation outlook consistent with the assumptions in the September SEP; see my recent note for a discussion of the December revision. By themselves, these changes would reduce 2023 core PCE inflation to 3.0 percent, ½ percentage point below the FOMC’s median December projections.

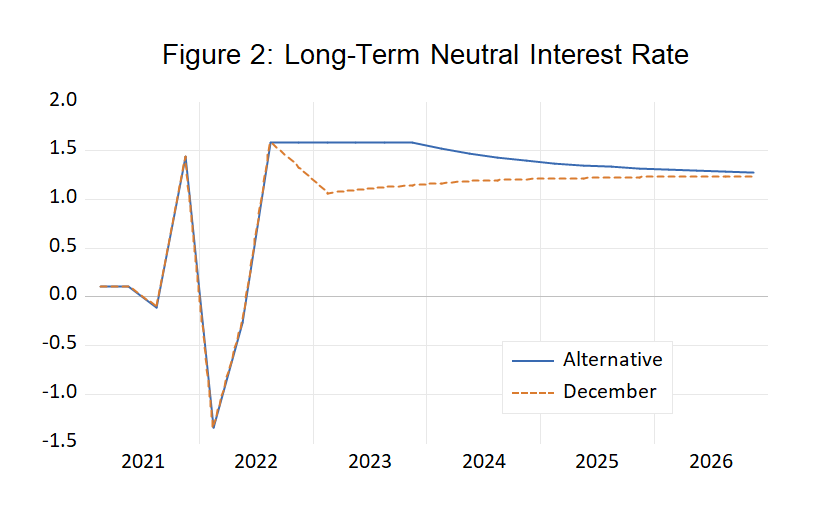

- For aggregate demand, I assume that the long-term neutral interest rate, a concept I’ve introduced in earlier posts, remains at a high level through the end of this year. By contrast, in my interpretation of the December SEP, this measure of the strength of aggregate demand implicitly retreated somewhat from the high level reached in the middle of last year.

- For monetary policy, I chose add-factors to the policy rule that bring the federal funds rate to 5.6 percent by the third quarter of this year, which corresponds to increases of 25 basis points at each FOMC meeting through July. I also boosted the persistence in the policy rule, from the value of 0.74 that had worked well in interpreting the December (and September) SEP paths, to 0.85. Without the near-term add-factors and increase in persistence, core inflation in 2025 would have been 2.4 percent.

Author: John Roberts, posted on https://jrobertsmacroecon.wordpress.com/2023/02/09/what-if-the-economy-remains-resilient/

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/john-roberts-what-if-the-economy-remains-resilient.html