There’s a new strategy in town that is making waves among retirees and the charitable organizations they support: donating a portion of your Individual Retirement Account (IRA) to fund gift annuities and receive a steady stream of income in return. This strategy, made possible by recent changes in legislation, is a win-win for both parties, offering significant tax benefits to the donor and a reliable source of funding for charities.

Background

Late last year, Congress passed a series of legislative changes affecting retirement savings. Starting from January 1, these changes allow retirees aged 70½ or older to donate up to $50,000 from their IRAs to fund gift annuities. This reform comes at an opportune time, coinciding with the retirement of the wealthiest generation in history, a significant portion of whose wealth is stored in retirement accounts.

In the past, donations to fund gift annuities could not be made directly from retirement accounts. This new law now facilitates such transactions, and charities are capitalizing on this change. Charitable organizations, from small liberal arts colleges to major entities like the American Red Cross and the Salvation Army, are encouraging their donors to fund gift annuities with their IRA dollars. The appeal lies not just in the charitable nature of the act, but also in the tax advantages and income generation potential it offers to retirees.

The Benefits

Let’s take the example of Catherine Ribnick, a retired Federal Deposit Insurance Corp. lawyer. She used the new law to donate $25,000 from her IRA to set up a gift annuity with Smith College, her alma mater. Ribnick’s annuity offers a fixed payout rate of 7%, which will provide her with $1,750 annually for the rest of her life. This not only helps to reduce the tax burden on her 2023 IRA required minimum distributions but also guarantees her a consistent income stream.

These gifts count towards the required minimum distributions (RMDs), the annual withdrawals that older Americans must make from their retirement accounts. Normally, these withdrawals are taxed as income, but when directed to charity, they become tax-free. Additionally, the charity agrees to make fixed annual payments to the donor, just like a traditional annuity purchased from an insurance company. Upon the donor’s death, any remaining money goes to the charity.

The Market

There are currently about 1,600 charities running gift annuity programs, with a total market value exceeding $4.4 billion. Given that Americans hold $11.5 trillion in IRAs, which constitute an increasing percentage of their overall financial assets, the potential for charitable gift annuities is vast. This is especially true as individuals begin to tire of the stock market’s volatility and seek the stability of a fixed income.

New Giving Opportunity

The new law combines IRA qualified charitable distributions with gift annuities, creating a unique giving opportunity. Here’s what you need to know:

Tax benefits

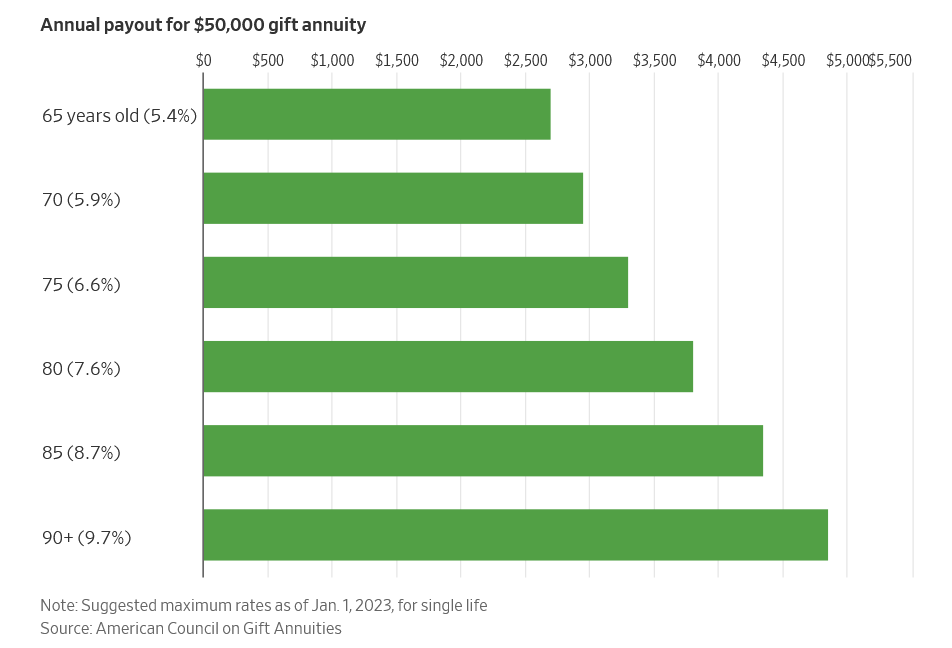

The IRA withdrawal doesn’t count as income, and it can count toward any required minimum distribution amount for the year. The IRA owner gets a minimum payout of 5% annually, taxed as ordinary income.

Restrictions

IRA-funded gift annuities come with special rules. A donor can make the gift in one tax year only. That could be one $50,000 gift, or several smaller gifts up to the $50,000 limit. The $50,000 amount counts toward a separate $100,000 limit per taxpayer for outright gifts to charity made with IRA dollars. The annuity can make payments to the donor or to the donor and spouse only. Payments have to start withina year of funding it.

Safety

The safety of a gift annuity depends on the financial stability of the charity. When a charity issues a gift annuity, it is pledging its assets to back it. As long as the charity remains financially sound, the annuity payments should continue unabated.

Rate Shopping

Yes, you can shop around for the best rate. Most charities use the American Council on Gift Annuities (ACGA) suggested payout rates, which have been revised upwards twice in the past year. These rates are based on a 50-50 split, with the charity expected to receive half of the initial donation amount upon the donor’s death. However, actual results show close to 70% going to charity, according to the ACGA.

In Summary

In essence, the new law presents a unique opportunity for retirees to make a significant charitable contribution, decrease their taxable income, and secure a fixed income stream. The emergence of IRA-funded gift annuities as a retirement strategy is a testament to the evolving dynamics of philanthropy and retirement planning.

This strategy isn’t just for the super-wealthy or philanthropically-inclined. It’s for anyone looking to navigate the complex waters of retirement finance strategically. By making smart choices about your IRA distributions, you can maximize your impact, reduce your tax liability, and secure a steady income for years to come.

Whether you’re tired of the stock market’s unpredictability or seeking a new way to support causes you care about, consider the potential benefits of IRA-funded gift annuities. It’s a retirement tax break that not only supports the charities you love but also pays you an annual income.

Retirement is a significant milestone and managing your finances during this phase is crucial. With the right information and planning, you can make the most of your retirement savings. An IRA-funded gift annuity is just one of many tools available to help ensure your golden years are both comfortable and fulfilling. As always, you should consult with a financial advisor or retirement expert to fully understand the implications of such a decision based on your personal circumstances and financial goals.

Ultimately, the new law offers a compelling strategy for those looking to balance philanthropy with financial stability in retirement. It’s a testament to the power of innovative legislation in creating win-win solutions for retirees and charitable organizations alike. The retirement tax break that pays you an annual income – it’s a proposition worth considering.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/maximize-your-impact-and-income-the-power-of-ira-funded-charitable-gift-annuities-in-retirement.html