As we enter the latter half of the year, government-bond yields have shown a discernible climb during the second quarter, fuelled by signals of robust economic vitality and a lessening of distress within the banking sector. Investors predict that these yields could continue their upward trajectory in the months to come.

In the opening months of the quarter, bonds were rallying as investors grappled with a series of swift banking collapses, sparking fears of a wider crisis that could impede the flow of money and credit to households and businesses. Despite these concerns, the economy and markets have demonstrated resilience amidst the turbulence, even as the government was engaged in a debt-ceiling standoff that almost resulted in default.

A series of recent reports indicate that the labor market is maintaining its strength even as inflation shows signs of diminishing. This has led to an increased optimism that the Federal Reserve can effectively control price increases without pushing the economy into a recession. However, analysts caution that the central bank’s significant rate hikes since early 2022 could start to act as a counterforce to growth in the upcoming months.

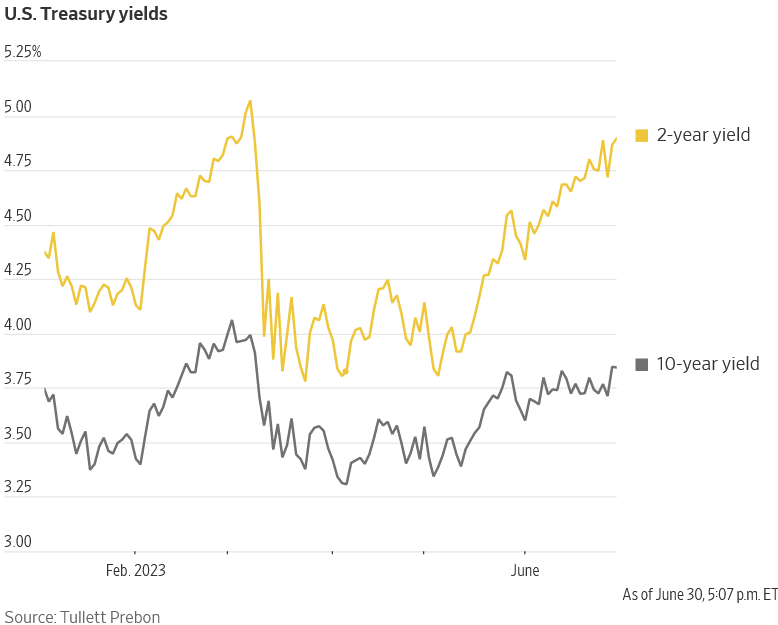

This renewed confidence has driven up the yields on Treasury bonds, which typically rise in tandem with expectations for economic activity, inflation, and how the Federal Reserve will adjust interest rates. The yield on the 10-year Treasury note concluded the quarter at 3.818%, up from 3.49% at the end of March. This increase in yield reflects a return to the levels seen at the start of the year, when the 10-year yield traded around 3.8%.

The U.S. government debt market, valued at approximately $30 trillion, serves as a crucial economic benchmark. Given the unlikelihood of the Treasury falling seriously behind on payments over the long term, Treasury yields effectively set a minimum on borrowing costs for consumers and businesses, impacting everything from the interest that companies pay on their bonds to the rates stamped on new mortgages.

Monetary policy set by the central bank deeply influences Treasurys. While the June Fed meeting concluded without an interest-rate hike for the first time since early 2022, the past quarter has seen a marked reassessment of the central bank’s future policy stance. Earlier in the year, futures markets indicated that investors were expecting several rate cuts by the end of 2023. This was based on fears that the unfolding banking crisis would necessitate intervention from the Fed to bolster a faltering economy. However, current market sentiment suggests that the Fed’s rate target will end the year higher than its present 5% to 5.25% level.

This shift in expectations has propelled 2-year Treasury yields, particularly sensitive to changes in the Fed’s interest-rate policy, to surge even more dramatically than their longer-term counterparts. The 2-year yield finished the quarter at 4.877%, up from 4.06% at the end of March. Notably, 2-year yields have consistently remained higher than 10-year yields for the past year, an unusual inversion of the normal yield curve that is often a precursor to a recession.

Despite this, Gennadiy Goldberg, head of U.S. rates strategy at TD Securities, warns that a slowdown remains a distinct possibility. “The market’s expecting this run of strong data to continue, but a lot of these things can start to unwind very quickly,” Goldberg cautioned, referring to the unusual rate-hiking cycle and the further inversion of the yield curve.

In an encouraging sign of renewed optimism, the recent rise in Treasury yields has not been paralleled by a similar uptick in corporate bond yields, which carry a higher risk due to the potential of bankruptcies. Instead, yields on company bonds have decreased relative to those on Treasurys,indicating a more optimistic outlook for business performance in the year ahead. Investment-grade corporate bonds now yield approximately 1.31 percentage points more than Treasurys, down from about 1.45 percentage points at the end of March, according to data from Intercontinental Exchange.

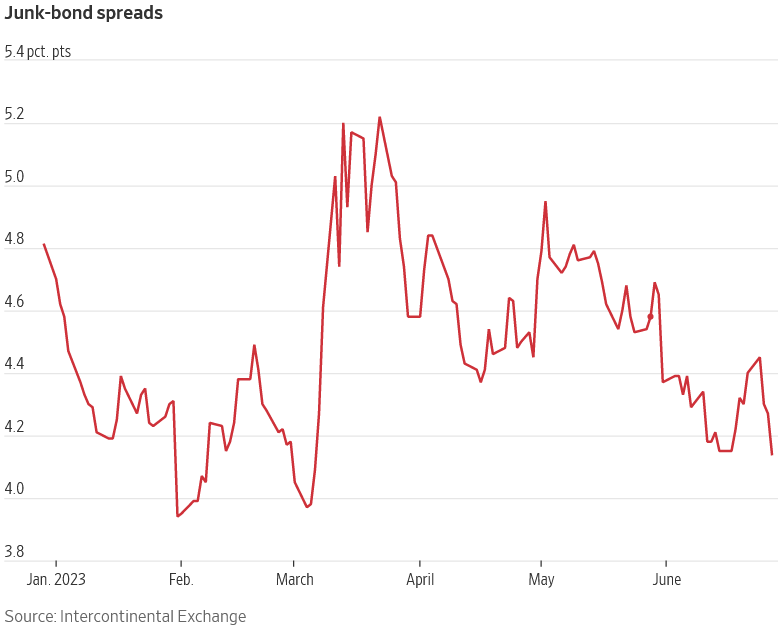

Moreover, the yield difference or spread on junk-rated bonds has also narrowed to 4.14 points from 4.58 points at the start of the quarter. This tightening of the spread suggests that investors perceive less risk in these bonds than before. While junk-bond defaults have been on the rise, Moody’s Investors Service predicts that they will peak at an annual rate of about 5% sometime next year. This estimated peak is below the levels typically observed during past downturns, signaling a more favorable environment for these higher-risk investments.

In recent weeks, regional banks such as Truist Financial have been successful in selling bonds with minimal pricing concessions, further signaling the improvement in investor sentiment. “The market seems like it’s in a totally different place than it was at the end of March,” said Blair Shwedo, head of investment-grade trading at U.S. Bank.

As we move forward, it is crucial to remember that markets are dynamic, and conditions can change rapidly. Despite the positive signs, caution and vigilance remain paramount, particularly given the potential repercussions of the unusual rate-hiking cycle and the inversion of the yield curve. With the economy and markets displaying resilience amidst turbulence, and investor sentiment on an upward trajectory, the stage is set for an interesting second half of the year.

Ultimately, the continued rise in Treasury yields reflects investor confidence in the economic growth story. However, as the inversion of the yield curve suggests, it’s a delicate balance between managing growth and staving off a potential recession. Investors and analysts alike will undoubtedly keep a close watch on the Federal Reserve’s moves and the unfolding economic indicators as they continue to navigate this intricate and evolving landscape.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/riding-the-yield-curve-how-treasury-bonds-signal-economic-optimism-amid-uncertainty.html