Introduction

In the ever-evolving landscape of finance and economics, one thing has become abundantly clear in recent years: the era of risk management suppression is coming to an end. The appetite for risk management is poised to surge in the coming years, and this transformation is primarily driven by a fundamental shift in central bank policies, notably the Federal Reserve (Fed) and the European Central Bank (ECB), as they pivot towards combating inflation and maintaining elevated short-term interest rates. In this blog post, we will explore the implications of this shift, its historical context, and the importance of embracing risk management in this new environment of positive real interest rates.

The Era of Suppressed Risk Management

To appreciate the significance of the changing tides, we must first understand the era of suppressed risk management that prevailed in the years leading up to 2022. This era was characterized by a prolonged period of historically low or negative real short-term interest rates, driven by the zero-interest-rate policy (ZIRP) initiated during the aftermath of the 2008 financial crisis. For over a decade, the prevailing sentiment among market participants was that central banks had their backs. This perception led to a culture of risk-taking, with mantras like “buy the dips” and “there is no alternative (to equities)” becoming popular among equity traders.

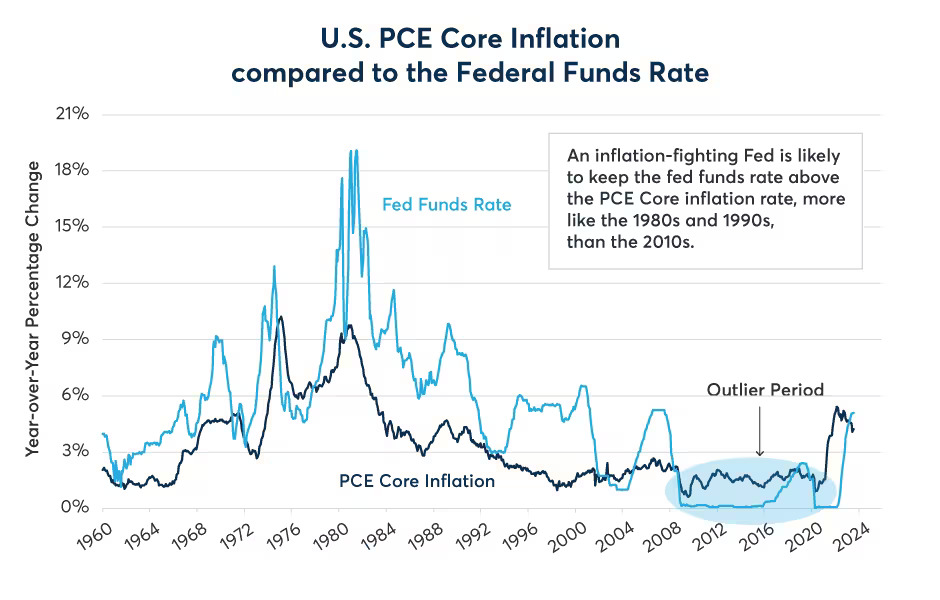

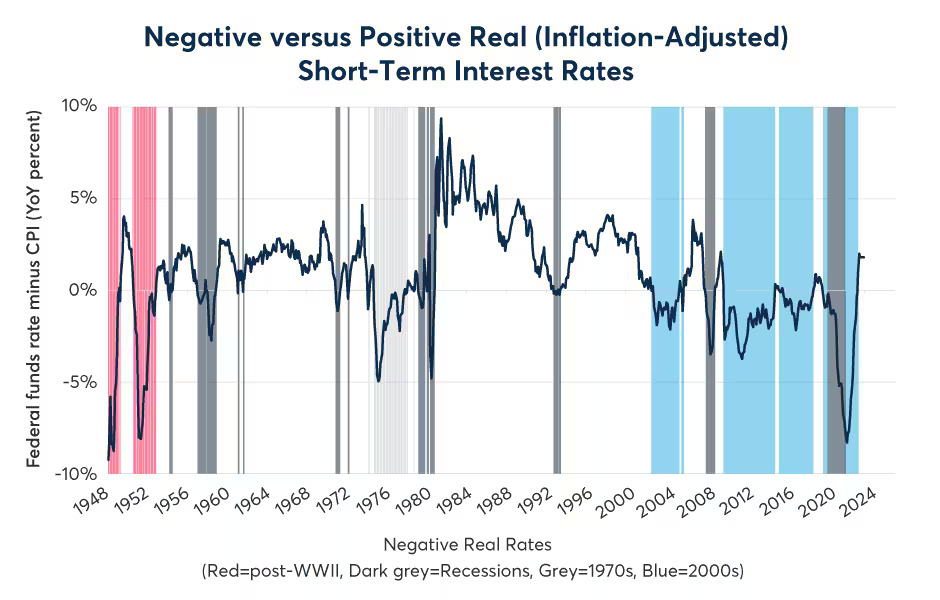

Historically, prior to the 2000s, the U.S. economy predominantly experienced overnight interest rates above the prevailing rate of inflation, resulting in positive real interest rates. However, the ZIRP era flipped this dynamic, with the Federal Funds rate staying below the year-over-year trailing Consumer Price Index (CPI) inflation rate for the majority of the time from 2009 to 2022. This shift in interest rate policy created an environment where the importance of risk management was severely underestimated.

The Career Context Bias

One significant challenge in recognizing the extent of risk management suppression during the ZIRP era is the “career context bias.” Many financial professionals and market participants have spent their entire careers within this environment, leading to a skewed perspective of what is considered normal. As a result, the true magnitude of risk management’s importance during the last two decades has been overlooked.

Quantitative Tightening (QT) and Price Discovery

The transition from quantitative easing (QE) to quantitative tightening (QT) represents another crucial aspect of the changing landscape. QE, characterized by central banks actively buying securities, distorted price discovery processes in both fixed income and equities. However, QT, which involves allowing the balance sheet to shrink as securities mature without active selling, does not have the same distorting effect. This transition has restored a more efficient price discovery system.

The Fed’s Reluctance to Change

Furthermore, the Federal Reserve’s reluctance to reverse course is an essential consideration. The Fed’s current trajectory involves raising interest rates, and a rate cut is unlikely until they are confident that a reversal is not necessary. This suggests a sustained period of positive real interest rates.

The 2% Core Inflation Target

The Fed’s unwavering commitment to maintaining a 2% core inflation target is another pivotal factor. Many of the factors that historically kept core inflation around 2% are changing or no longer applicable, making this target more challenging to achieve. This firm stance on inflation targeting has significant implications for the future economic landscape.

Embracing Risk Management in a New Era

In light of these considerations, it becomes evident that the suppression of risk management during the ZIRP era was of exceptional magnitude. As central banks shift their focus towards fighting inflation and maintain positive real interest rates, the economic system will inherently carry more risk. This necessitates a fundamental shift in the approach of economic agents, including investors, traders, financial institutions, and commercial enterprises, towards risk management as a critical component of future success.

Conservation of Risk

The concept of the “conservation of risk” is essential to grasp. Risk does not disappear but rather shifts within a complex economic system. Suppressing risk in one area often leads to its emergence in another. Therefore, allowing economic agents to efficiently manage their risks in an environment of positive real interest rates could lead to a more optimal allocation of capital and promote long-term economic growth.

Conclusion

The era of risk management suppression, characterized by prolonged periods of negative real interest rates, is coming to an end. Central banks’ shift towards combating inflation and maintaining positive real interest rates signals a new era where the importance of risk management cannot be overstated. Financial market participants, institutions, and businesses must adapt to this changing landscape, recognizing that efficient risk management will be a cornerstone of future success. As we move forward, embracing this new paradigm may ultimately benefit the economy by allowing for more effective allocation of capital and promoting sustainable growth.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/navigating-the-new-era-the-end-of-risk-management-suppression.html