In a surprising economic twist, many Americans who saw a significant jump in their credit scores during the early stages of the pandemic are now stumbling on loan payments at a higher-than-expected rate. This pattern is presenting a complex challenge for lenders and borrowers alike, as they navigate through the quagmire of pandemic-induced financial repercussions.

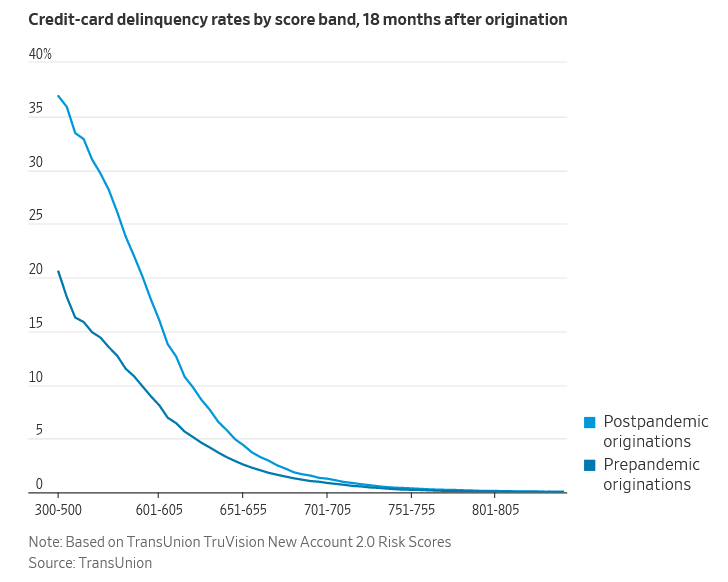

An analysis by TransUnion, a leading credit-reporting company, revealed a startling correlation between increased credit scores and delinquency rates. The study, which examined over 75 million scores, showed that delinquency rates for credit cards and personal loans opened in mid-2021 resembled those of borrowers with credit scores 25 points lower in the first quarter of 2023. For auto loans, the delinquency rates were akin to borrowers with credit scores that were 10 points lower.

For decades, lenders have used credit scores as a primary barometer to evaluate the potential risks associated with granting loans. The scores, which rank borrowers on the likelihood that they will repay, have been pivotal in determining who can obtain a mortgage, personal loan, car loan, or other credit facilities. But the advent of the pandemic has introduced a disjointed relationship between credit scores and actual financial situations, complicating risk assessment for lenders.

Despite looming warnings about a potential recession and the Federal Reserve’s aggressive rate hikes, the economy remains relatively stable. However, the rising delinquency rates may portend the onset of future financial hardships.

The increasing cost of housing, cars, and packaged goods is exerting pressure on many household budgets, despite a general easing of inflation. Concurrently, more borrowers are deferring balances each month rather than paying them off entirely, a practice that, coupled with higher interest rates, is causing an uptick in monthly payments on credit cards and other loans.

Interestingly, credit scores experienced a widespread increase early in the pandemic, despite rampant unemployment. Thanks to stimulus checks, unemployment benefits, and widespread pauses on mortgages and student loans, many borrowers had a surplus of money. The decrease in commuting, eating out, and traveling expenses further allowed them to save and pay down their debts.

Data from Intuit Credit Karma reveals that over a quarter of subprime borrowers with credit scores below 600 at the onset of the pandemic had ascended to near-prime status by mid-2021, with an average score increase of 88 points.

However, this upward credit score trajectory has begun to reverse. These borrowers’ average credit card and personal loan balances have escalated past their pre-pandemic levels by this spring. Approximately 38% of these borrowers have slipped back into subprime territory, experiencing an average credit score decline of more than 90 points.

The peculiar trend of inflated credit scores and subsequent decline has prompted lenders to consider factors beyond credit scores when evaluating loan applicants. Brendan Coughlin, the head of the consumer-banking division at Citizens Financial Group, noted that the pandemic had artificially inflated credit scores. He pointed out that under normal economic conditions, more people might have tipped into the danger zone.

In response, Citizens Financial Group has invested heavily in technology that could provide additional insights to inform its credit decisions. They have poured millions into developing advanced internal score models and other analytical tools.

Coughlin emphasized, “We needed more information to have confidence in how we were underwriting.” This statement is indicative of an industry-wide shift towards a more comprehensive and nuanced approach to credit evaluation.

The intertwining of pandemic-induced economic factors and credit score changes presents a unique set of challenges. As financial institutions adapt and evolve their lending criteria, borrowers must also navigate these uncharted waters, equipping themselves with financial knowledge and resilience. This tumultuous economic period is likely to leave lasting impacts on credit practices, prompting all stakeholders to reassess and adapt their strategies.

In conclusion, the unprecedented economic disruptions caused by the pandemic have illuminated the limitations of credit scores as a standalone indicator of financial risk. It has led to a situation where an initial rise in credit scores, bolstered by pandemic relief measures, has given way to increasing delinquencies as financial realities catch up. As a result, lenders are being compelled to seek more comprehensive tools for risk assessment, moving beyond the traditional reliance on credit scores.

The trajectory of these credit score fluctuations, and the consequent borrowing patterns, underscore the complex dynamics of our financial ecosystem during times of crisis. It serves as a stark reminder that credit scores, while helpful, may not capture the full picture of an individual’s financial health, especially in a volatile economic landscape.

For borrowers, this situation highlights the importance of maintaining a holistic approach to financial health, one that extends beyond merely managing their credit scores. Fostering good financial habits such as saving, budgeting, and timely debt repayment, coupled with staying informed about the changing lending landscape, can equip borrowers to navigate any economic situation resiliently.

For lenders, the challenge lies in refining and diversifying risk assessment methods to capture the full breadth of a borrower’s financial situation, thereby making more accurate predictions about loan repayment.

As we continue to grapple with the lingering effects of the pandemic and its impact on the economy, it becomes more crucial to learn, adapt, and innovate. With an open mind and a willingness to evolve, both lenders and borrowers can navigate through this complex scenario to foster a more robust and resilient financial environment.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/the-paradox-of-pandemic-inflated-credit-scores-and-rising-delinquencies.html