A credit score is a numerical rating that represents an individual’s creditworthiness. It is a measure of how likely a person is to repay a loan or credit card debt on time. A credit score is based on a person’s credit history and is used by lenders, landlords, insurers, and others to evaluate an individual’s ability to manage their financial obligations. A credit score is used to predict a borrower’s risk level in repaying a debt. The higher a person’s credit score, the less risk they are considered to be, and thus, the more likely they are to be approved for loans, credit cards, and other forms of credit.

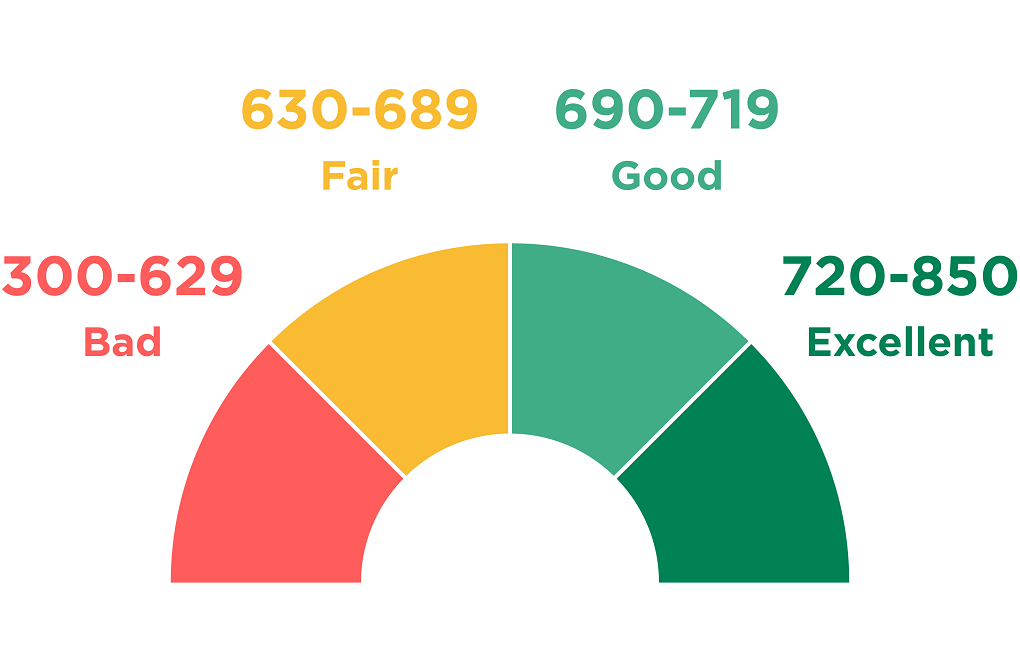

The most widely used credit score in the United States is the FICO score, which ranges from 300 to 850. The higher your FICO score, the better your credit rating is considered. A score of 700 or higher is generally considered good, while a score of 750 or higher is considered excellent. A score below 600 is considered poor.

A credit score is a numerical rating that represents an individual’s creditworthiness. It’s used by lenders, landlords, insurers, and others to evaluate an individual’s ability to manage their financial obligations. The most widely used credit score in the United States is the FICO score, which ranges from 300 to 850. Your credit score is calculated based on a number of factors, including payment history, credit utilization, length of credit history, types of credit and recent credit inquiries. It’s important to check your credit score regularly and take steps to improve it if necessary.

Your credit score is one of the most important figures in your financial life. It can determine whether you can get a loan, how much you can borrow, and even the kinds of jobs you can get. Understanding your credit score and how it affects your financial future is key to making smart financial decisions and creating a secure financial future.

Understanding Your Credit Score

Your credit score is a three digit number that ranges from 300 to 850 and is based on information from your credit report. It is used by lenders to determine your creditworthiness, which is a measure of how likely you are to pay back a loan. The higher your credit score, the more likely you are to be approved for a loan or credit card and the better terms you will get.

Why Credit Scores Matter

Your credit score can have a huge impact on your financial life. It is used by lenders to determine whether or not to approve you for a loan or credit card, how much you can borrow, and what interest rate you will pay. In addition, landlords, employers, and insurance companies may use your credit score to make decisions about you. A good credit score can help you get the things you need and want, while a poor credit score can make it more difficult or even impossible to get a loan, credit card, or job.

The Effects of Poor Credit Scores

Having a poor credit score can have serious consequences. You may be denied a loan or credit card, or you may be approved but with a higher interest rate and higher fees. In addition, you may have to put down a larger down payment on a car or house or pay higher insurance premiums. Poor credit can also hurt your chances of getting certain jobs and make it more difficult to rent an apartment.

Improving Your Credit Score

The first step to improving your credit score is to get a copy of your credit report and check it for errors. You can do this for free using AnnualCreditReport.com. Once you’ve checked your credit report, you can begin to take steps to improve your credit score. This can include paying your bills on time, reducing your debt, and not applying for new credit unless absolutely necessary.

Benefits of Good Credit

Having a good credit score can have many benefits. You are more likely to be approved for loans and credit cards with better terms and lower interest rates. You may also be able to qualify for better rates on mortgages, car loans, and other types of financing. In addition, a good credit score can make it easier to rent an apartment and get certain jobs.

Steps to Take to Get Your Credit Score Back on Track

If you have a poor credit score, there are steps you can take to improve it. The first step is to check your credit report for errors and take steps to correct them. You should also make sure you are paying your bills on time and reducing your debt. In addition, try to limit the number of times you apply for new credit and don’t close old accounts.

How to Monitor Your Credit Score

You should regularly monitor your credit score to make sure it is accurate and up to date. You can do this for free using AnnualCreditReport.com or by signing up for a credit monitoring service. By monitoring your credit score, you will be able to spot any potential errors or fraudulent activity and take steps to correct them.

It is important to check your credit score regularly to make sure there are no errors and to monitor your credit history. If you notice any errors, you can contact the credit bureau to have them corrected. Also, you can take steps to improve your credit score, such as paying your bills on time, keeping your credit utilization low, and limiting the number of credit inquiries you make.

Credit Score Myths Debunked

There are many myths about credit scores circulating. It is important to understand the truth so you can make informed decisions about your finances. One myth is that you need to carry a balance on your credit cards in order to have a good score. However, this is not true. Paying off your balance in full each month is actually better for your credit score.

Credit scores are calculated using a complex algorithm that takes into account a variety of factors, including payment history, credit utilization, length of credit history, types of credit, and recent credit inquiries. Payment history and credit utilization are considered to be the most important factors. Payment history includes whether you have paid your bills on time and whether you have any outstanding debts in collections. Credit utilization is the amount of credit you are using compared to your credit limit.

Managing Credit and Debt Wisely

It is important to manage your credit and debt wisely in order to maintain a good credit score. You should make it a priority to pay your bills on time, limit the amount of debt you take on, and not apply for too much new credit. Additionally, you should use your credit wisely and only borrow what you can afford to pay back.

Financial Tips for Building Credit

Building a good credit score takes time and effort. Here are a few tips to help you get started:

- 1. Pay your bills on time.

- 2. Pay off your debt.

- 3. Don’t open too many accounts at once.

- 4. Keep your credit utilization low.

- 5. Monitor your credit score regularly.

Conclusion

Your credit score is an important factor in your financial life. It can determine whether you are approved for loans and credit cards, what kind of interest rates you will pay, and even what kind of job you can get. It is important to understand how your credit score works and how to maintain a good score in order to get the best terms and rates available.

Top Ten Key Takeaways

1. Your credit score is a three digit number that ranges from 300 to 850 and is based on information from your credit report.

2. Your credit score is used by lenders to determine your creditworthiness and can affect your ability to get loans, credit cards, and even jobs.

3. Poor credit can lead to higher interest rates and fees, or may even make it impossible to get a loan or credit card.

4. You can improve your credit score by paying your bills on time, reducing your debt, and limiting the number of times you apply for new credit.

5. A good credit score can help you get better terms and rates on loans and credit cards, as well as better job opportunities.

6. You can get a free copy of your credit report and check it for errors.

7. You should regularly monitor your credit score to make sure it is accurate and up to date.

8. There are many myths about credit scores circulating; make sure you understand the truth about credit scores.

9. Managing your credit and debt wisely is key to maintaining a good credit score.

10. Building a good credit score takes time and effort; make sure you are taking the necessary steps to improve your score.

Your credit score is an important factor in your financial life and is key to making smart financial decisions and creating a secure financial future. Take the time to understand how credit scores work and how to maintain a good score so you can get the best terms and rates available.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/the-impact-of-credit-scores-on-your-financial-future.html