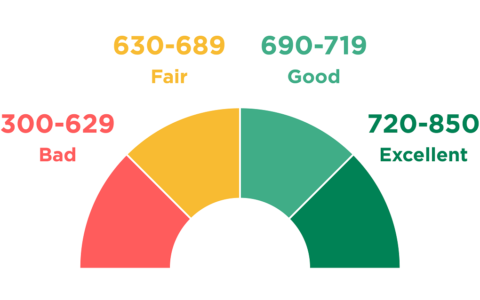

Your credit score is an important measure of your financial health, influencing everything from the interest rates you pay on loans to your ability to rent an apartment or get a job. While many people are aware that missing payments or carrying high levels of debt can damage their credit score, there are some surprising factors that can also have a negative impact. Here are 7 surprising things that can damage your credit score.

Canceling a Credit Card

Canceling a credit card can potentially hurt your credit score in a few ways. First, canceling a credit card reduces your overall available credit, which can increase your credit utilization rate. This rate is the percentage of your available credit that you are currently using. A high credit utilization rate can lower your credit score because it suggests that you may be overextended financially and have a higher risk of defaulting on your debts.

Secondly, canceling a credit card can also impact the length of your credit history. The length of your credit history is a factor used in calculating your credit score, with a longer credit history generally viewed more favorably. If you cancel a credit card that you’ve had for a long time, it can shorten your credit history, which may lower your credit score.

However, if you cancel a credit card that has an annual fee and you don’t use it anymore, it may be worth it to avoid paying the fee. Additionally, if you cancel a credit card and have other lines of credit that you have responsibly managed, the impact on your credit score may be minimal.

Applying for Too Much Credit

Applying for too much credit within a short period of time can potentially hurt your credit score. Each time you apply for credit, a lender will typically request a copy of your credit report and credit score from a credit bureau. This request is called a “hard inquiry” and it is recorded on your credit report.

If you have too many hard inquiries on your credit report within a short period of time, it can suggest to lenders that you are taking on too much debt or that you may be in financial trouble. This can lower your credit score and make it more difficult to obtain credit in the future.

However, not all credit inquiries are created equal. There are also “soft inquiries” which are not recorded on your credit report and do not affect your credit score. Soft inquiries can occur when you check your own credit report, when a lender pre-approves you for credit, or when a creditor or employer checks your credit as part of a background check.

Too many credit card applications

Applying for too many credit cards within a short period of time can potentially hurt your credit score. When you apply for a credit card, the credit card issuer will typically request your credit report from one or more of the major credit bureaus. This results in a hard inquiry on your credit report, which can lower your credit score.

If you apply for multiple credit cards within a short period of time, this can indicate to lenders that you are seeking a lot of credit all at once, which can make you appear higher risk. This can result in a lower credit score and may make it more difficult for you to obtain credit in the future.

However, it’s important to note that not all credit inquiries have the same impact on your credit score. If you are shopping around for the best credit card offer and apply for multiple credit cards within a short period of time, the credit bureaus may recognize this as a single inquiry and only count it as one hard inquiry on your credit report.

Car rental reservations

If you’re planning to rent a car, you should be aware that using a debit card to make the reservation might prompt the rental car company to perform a credit screening. This inquiry could negatively impact your credit score. An alternative option is to use your credit card to confirm the reservation and avoid the unnecessary credit inquiry. When returning the vehicle, you can then settle the final bill with your debit card.

Past-due rent payments

Late or past-due rent payments can have a negative impact on your credit score. Many landlords and property management companies report late rent payments to credit bureaus, which can lower your credit score and make it more difficult to obtain credit in the future.

While rent payments are not typically reported to credit bureaus unless they are more than 30 days late, even a single late payment can still have a negative impact on your credit score. If you are struggling to make your rent payments, it’s important to communicate with your landlord and try to work out a payment plan to avoid damaging your credit score.

Additionally, there are some services that can help renters build their credit by reporting their rent payments to credit bureaus. By using these services and making timely rent payments, renters can improve their credit score and establish a positive credit history.

So, paying your rent on time is not only important for avoiding late fees and eviction, but also for maintaining a good credit score. Late or past-due rent payments can have a negative impact on your credit score, so it’s important to communicate with your landlord and take steps to make timely payments. By doing so, you can protect your credit score and establish a strong credit history.

Co-Signing for Someone Else

Co-signing for someone else can potentially hurt your credit score in a few ways. When you co-sign a loan or credit card, you are agreeing to be equally responsible for the debt with the other person. This means that if the other person misses payments or defaults on the debt, it can impact your credit score as well as theirs.

Firstly, the co-signed debt will appear on your credit report as well as the other person’s. This means that if the other person misses payments or defaults on the debt, it will show up as a negative mark on your credit report, potentially lowering your credit score.

Secondly, co-signing for someone else can impact your debt-to-income ratio. This ratio is the percentage of your monthly income that goes toward paying your debts. If the co-signed debt is large, it can increase your debt-to-income ratio, which can lower your credit score and make it more difficult to obtain credit in the future.

However, if the other person makes all payments on time and the debt is paid off in full, co-signing can potentially help your credit score by showing a positive credit history and reducing your debt-to-income ratio.

In conclusion, co-signing for someone else can potentially hurt your credit score by increasing your debt-to-income ratio and causing negative marks on your credit report if the other person misses payments or defaults on the debt. It’s important to carefully consider the potential impact on your credit score before co-signing for someone else. If you decide to co-sign, make sure you have a plan in place to ensure the debt is paid off in full and on time to minimize any negative impact on your credit score.

Defaulting on recurring bills

Defaulting on recurring bills can hurt your credit score in a few ways. When you sign up for a recurring bill, such as a phone or utility bill, you are entering into a contract to make regular payments. If you miss or are late on these payments, it can negatively impact your credit score.

Firstly, if you miss a payment, the company may report the late payment to the credit bureaus. This can result in a negative mark on your credit report, which can lower your credit score.

Secondly, if you continue to miss payments, the company may turn your account over to a collection agency. This can result in even more negative marks on your credit report, which can further lower your credit score.

Finally, if the account is turned over to a collection agency and the debt remains unpaid, the agency may take legal action against you. This can result in a judgment against you, which will also appear on your credit report and negatively impact your credit score.

Breached gym membership contracts

Breached gym membership contracts can potentially hurt your credit score in a few ways. When you sign up for a gym membership, you are entering into a contract to pay for services on a regular basis. If you breach this contract by not paying, it can have negative consequences for your credit score.

Firstly, the gym may report your missed payments or breach of contract to the credit bureaus. This can result in a negative mark on your credit report, which can lower your credit score.

Secondly, the gym may turn your account over to a collection agency, which can further damage your credit score. If the collection agency reports the delinquent account to the credit bureaus, it can result in additional negative marks on your credit report.

Finally, if the debt remains unpaid and the collection agency takes legal action against you, it can result in a judgment against you, which will also appear on your credit report and negatively impact your credit score.

Large outstanding medical bills

Large outstanding medical bills can potentially hurt your credit score in a few ways. When you receive medical treatment, you are responsible for paying for the services you receive. If you have a large outstanding medical bill, it can have negative consequences for your credit score.

Firstly, the medical provider or facility may report your missed payments or outstanding debt to the credit bureaus. This can result in a negative mark on your credit report, which can lower your credit score.

Secondly, if the outstanding medical bill is turned over to a collection agency, it can further damage your credit score. If the collection agency reports the delinquent account to the credit bureaus, it can result in additional negative marks on your credit report.

Finally, if the debt remains unpaid and the collection agency takes legal action against you, it can result in a judgment against you, which will also appear on your credit report and negatively impact your credit score.

In conclusion, your credit score is a valuable asset that can impact your financial health in many ways. Avoiding these surprising credit score killers can help you maintain a healthy credit score and achieve your financial goals. By staying vigilant, checking your credit report regularly, and using credit responsibly, you can keep your credit score in good shape and enjoy the many benefits that come with a strong credit history.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/watch-out-9-unexpected-actions-that-can-harm-your-credit-score.html