Over the past few weeks, global markets have been shaken by rising geopolitical tensions, particularly in the Middle East. When headlines intensify and uncertainty rises, investors naturally begin asking the same familiar questions: Should I move some assets to cash? Should I buy energy stocks? Should I rotate into defensive sectors?

These reactions are understandable. Geopolitical conflicts have historically triggered sharp moves in oil prices, currency markets, and global equities. But reacting to headlines alone can lead investors to misinterpret what the market is actually signaling.

A closer look at the data reveals a more nuanced picture. While headlines emphasize risk, several underlying indicators suggest the market may be more resilient than many investors believe. In fact, some of the most interesting signals right now are surprisingly constructive.

Below are five key takeaways from the recent market volatility, along with an additional quiet positive development that investors may be overlooking.

1. The Market May Already Be Pricing in More Fear Than Investors Realize

At first glance, the current market environment may appear complacent. U.S. stocks have delivered three consecutive years of above-average returns, and valuation metrics such as price-to-earnings (P/E) ratios remain above their long-term averages.

This has led many investors to conclude that markets are overly optimistic.

However, beneath the surface, several indicators suggest the opposite: investor anxiety is already quite elevated.

One of the clearest signals is the VIX index, often referred to as the market’s “fear gauge.” Since the recent Middle East tensions began escalating, the VIX has surged into the top decile of its historical range, indicating unusually high levels of expected volatility.

Another indicator comes from valuation spreads, which measure the difference between the valuations of the most expensive stocks and the cheapest ones. These spreads have also widened significantly, another classic sign of investor nervousness.

Interestingly, the bond market is not displaying the same level of stress.

The key indicator there is credit spreads, which represent the extra yield investors demand for holding corporate bonds instead of safer government debt. While credit spreads have widened slightly since geopolitical tensions rose, they remain far from levels historically associated with financial distress.

This divergence matters. Historically, the credit market often provides a more measured view of economic risks, while the stock market tends to react quickly to headlines.

When stocks appear fearful but credit markets remain calm, it often creates the kind of environment where equities “climb the wall of worry.” In other words, much of the bad news may already be priced into stocks.

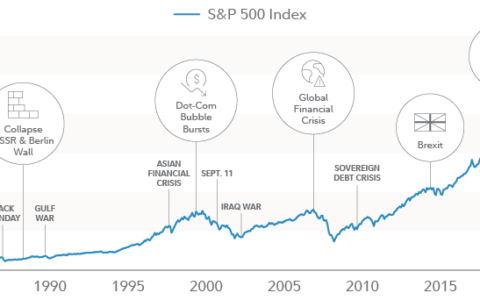

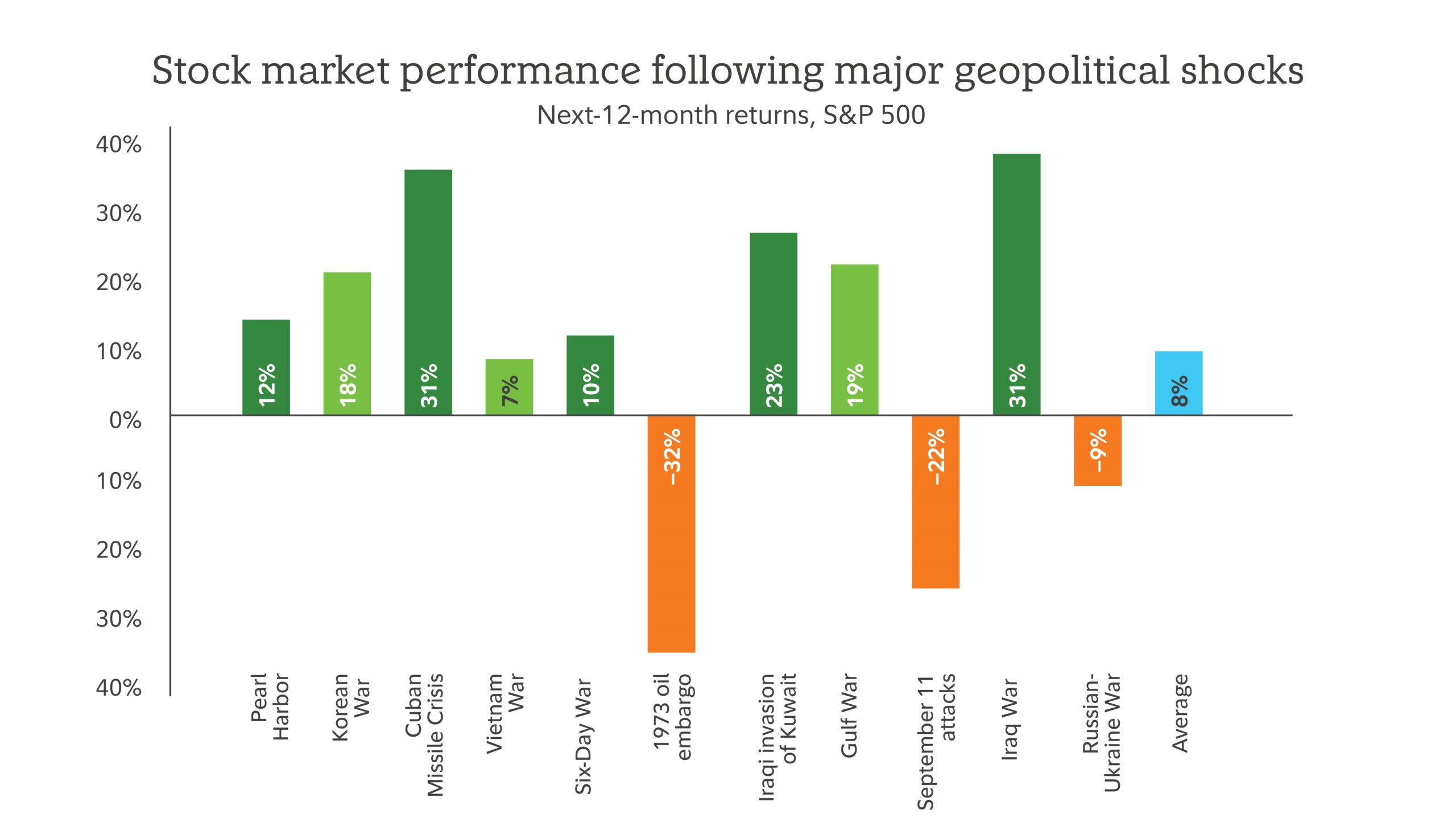

2. Geopolitical Shocks Rarely Derail Long-Term Market Performance

Geopolitical conflicts understandably create anxiety for investors. From wars to terrorist attacks to diplomatic crises, such events dominate headlines and often trigger short-term market swings.

But history offers an important perspective: geopolitical shocks rarely derail the stock market over the long run.

When researchers examine major geopolitical events—from Pearl Harbor to the Gulf War to the Russia-Ukraine conflict—the average stock market return in the 12 months following the event is roughly in line with the long-term historical average of around 8%.

This doesn’t mean markets ignore geopolitical developments. In the short term, volatility often increases. But markets tend to adapt quickly as investors reassess the economic impact.

In many cases, markets recover faster than expected because businesses, governments, and global supply chains adjust.

The lesson for investors is clear: reacting aggressively to geopolitical headlines often leads to poor timing decisions. Investors who sell during moments of panic frequently miss the recovery that follows.

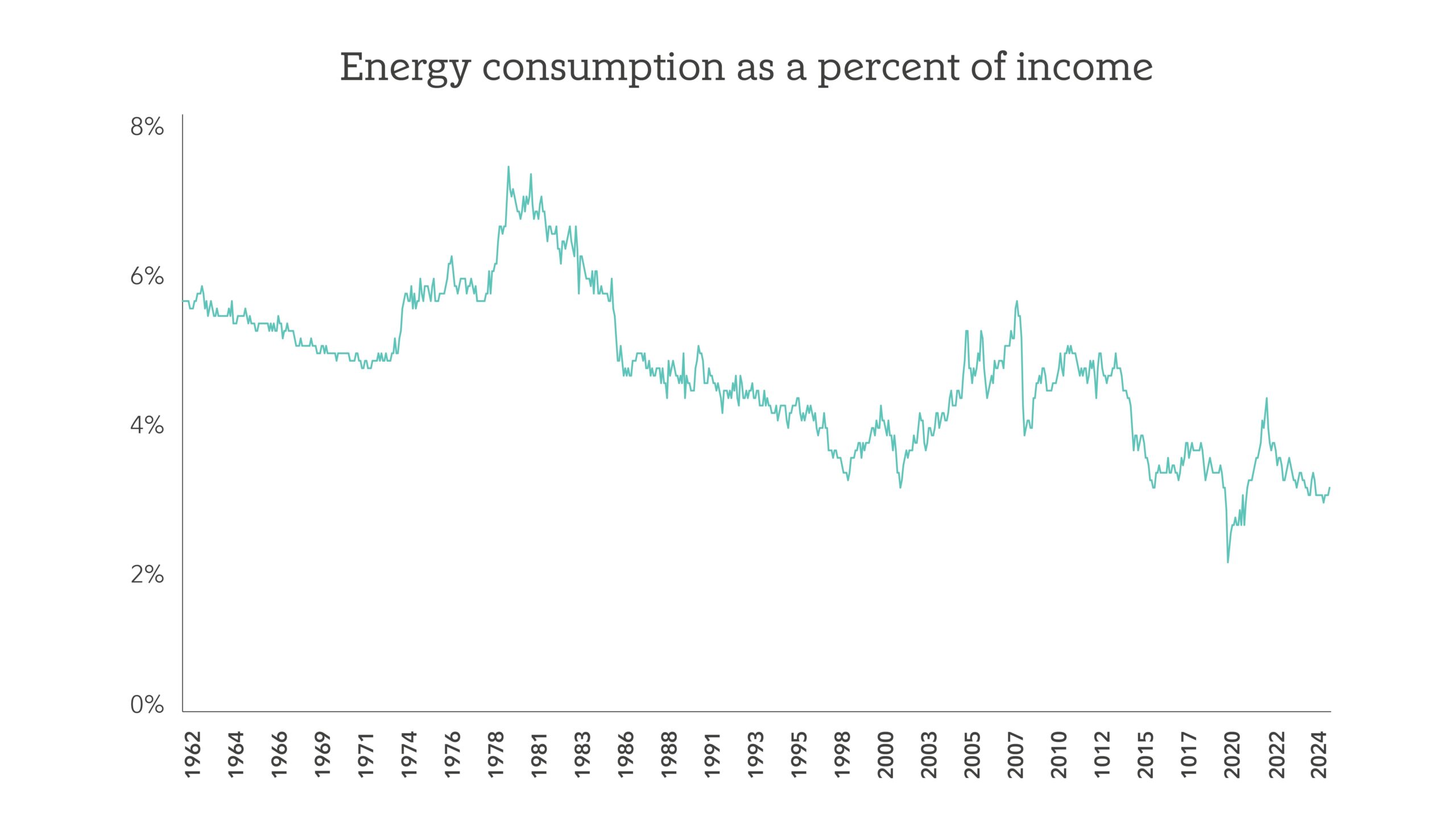

3. The Energy Shock Today Is Very Different from the 1970s

When geopolitical conflicts do significantly affect financial markets, the transmission channel is often energy prices.

The most famous example is the 1973 oil embargo, when the Organization of the Petroleum Exporting Countries (OPEC) sharply restricted oil supplies. The resulting spike in oil prices contributed to high inflation, economic slowdown, and weak stock market returns.

However, today’s global energy landscape is dramatically different.

First, the world is less dependent on Middle Eastern oil than it was in the 1970s. Production from countries within the OECD, particularly the United States, has increased significantly due to the shale revolution.

Since 2020, the United States has become a net exporter of crude oil, a historic shift from its previous role as a major importer.

Second, the share of household income spent on energy has fallen significantly. In the 1970s, Americans spent roughly 8% to 9% of their income on energy. Today that figure is closer to 3%.

This difference dramatically reduces the economic damage caused by rising energy prices.

Historically, economic strain tends to occur when household energy spending rises to roughly 5% of income or higher. Based on current data, that threshold would likely correspond to oil prices in the range of $135 to $145 per barrel—well above recent levels.

In other words, oil prices would likely need to rise substantially and remain elevated for an extended period before triggering the kind of economic slowdown seen in past energy crises.

4. Oil Prices Often Fall After Geopolitical Shocks

One of the most surprising historical patterns is that oil prices frequently decline in the year following major geopolitical shocks.

This may seem counterintuitive. When news breaks about attacks on energy infrastructure, disruptions in shipping routes such as the Strait of Hormuz, or reduced production from oil-exporting countries, investors naturally assume prices will continue rising.

Yet historically, oil markets often behave differently.

There are several reasons for this pattern.

First, markets frequently price in geopolitical risks before they fully materialize. In the current situation, oil prices had already been trending higher in the months leading up to the latest conflict.

Second, high prices tend to stimulate new supply and reduce demand. Energy producers may increase production, governments may release strategic reserves, and consumers may reduce consumption.

Economists often summarize this dynamic with a simple phrase: “high prices cure high prices.”

This does not mean oil prices will immediately fall. Short-term movements remain highly unpredictable, and volatility may continue. However, history suggests that investors should avoid assuming that energy prices will rise indefinitely following geopolitical shocks.

5. Sector Leadership Is Sending an Unexpected Signal

Perhaps the most interesting takeaway from recent market movements is the unexpected leadership among sectors.

Many investors assumed energy stocks would dramatically outperform as oil prices rose and geopolitical tensions intensified. Energy did outperform the S&P 500 during the week following the escalation of conflict, but only modestly.

The real standout sector was software, which delivered the strongest performance during the same period. The broader technology sector also performed well.

This leadership is noteworthy because technology valuations had previously compressed relative to the broader market.

Quantitative research shows that relative valuations for the tech sector have fallen into the lower third of their historical range. When similar valuation conditions occurred in the past, the sector went on to outperform approximately 70% of the time.

Within technology, the valuation gap appears especially large in software companies. Operating profit margins remain strong, yet relative valuations have fallen to historically low percentile levels.

Some investors worry that artificial intelligence may disrupt traditional software companies, potentially rendering certain business models obsolete.

While disruption is always possible, many companies may adapt and incorporate AI into their products, creating new sources of value. Current valuations may therefore provide a margin of safety against both technological disruption and macroeconomic risks.

A Quiet Positive: Manufacturing May Be Improving

One of the most overlooked developments in the current economic landscape is a potential rebound in U.S. manufacturing.

Recent data from the manufacturing purchasing managers’ index (PMI) shows two consecutive months of expansion, suggesting that the sector may be emerging from several years of sluggish performance.

Manufacturing has been a weak spot in the U.S. economy for much of the past decade. If the current improvement proves durable, it could provide an additional tailwind for economic growth, corporate profits, and overall market performance.

This development receives far less attention than geopolitical headlines, but it could ultimately prove more important for investors.

Conclusion: Markets Often Tell a More Balanced Story Than Headlines

In times of geopolitical tension, investors naturally focus on risks. News coverage tends to emphasize worst-case scenarios, and fear can spread quickly through financial markets.

But the data often tells a more balanced story.

Right now, several indicators suggest the situation may not be as dire as headlines imply:

- Fear is already heavily priced into equities

- Credit markets remain relatively calm

- The global economy is less vulnerable to oil shocks than in the past

- Oil prices often fall after geopolitical spikes

- Technology sectors may be regaining leadership

- U.S. manufacturing may be quietly improving

None of this eliminates uncertainty. Markets can still experience volatility, and geopolitical developments remain difficult to predict.

However, investors who step back and analyze the data rather than reacting emotionally to headlines often gain a clearer perspective.

History repeatedly shows that markets are remarkably resilient. For long-term investors, maintaining discipline and focusing on fundamentals rather than short-term noise remains one of the most effective strategies for navigating turbulent times.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/5-key-market-takeaways-from-recent-volatility-what-investors-should-understand-about-stocks-oil-and-sector-leadership.html