Building long-term wealth is rarely about one big decision—it’s about consistently making smart financial moves over time. Among the most effective tools available to investors in the United States is the Individual Retirement Account (IRA), a tax-advantaged vehicle designed to help you grow your savings efficiently.

Whether you’re just starting your career, self-employed, or already contributing to a workplace retirement plan, an IRA can play a critical role in strengthening your financial future.

For the 2025 tax year, the contribution window remains open until April 15, 2026, offering investors a valuable opportunity to take action. Below are three compelling reasons why contributing to an IRA now can significantly benefit your long-term financial plan.

1. Put Your Money to Work Early and Harness the Power of Compounding

One of the most powerful forces in investing is compound growth—the ability for your money to generate earnings, and then for those earnings to generate even more earnings over time.

An IRA provides a structured environment where compounding can truly shine.

Contribution Limits and Flexibility

For the 2025 tax year:

- You can contribute up to $7,000, or your total taxable earned income (whichever is less)

- If you’re age 50 or older, you can contribute up to $8,000

- Married couples filing jointly may also enable a nonworking spouse to contribute, provided household income meets requirements

These limits create a meaningful opportunity to systematically build retirement savings.

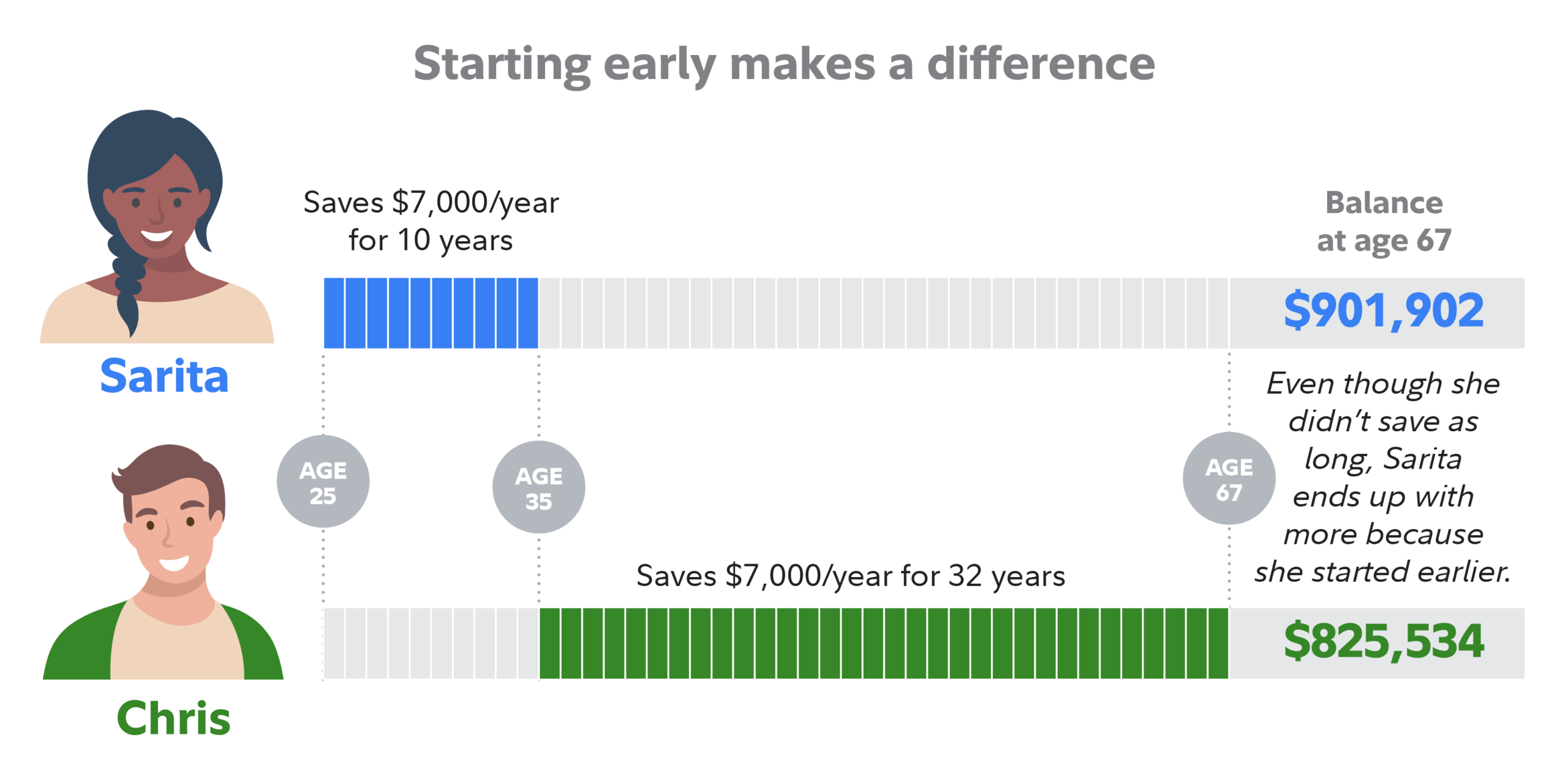

Why Starting Early Matters

Time is the most valuable asset in investing. Even modest contributions can grow substantially when given enough time.

Consider this principle:

- An investor who contributes early—even for a shorter period—may accumulate more wealth than someone who starts later but contributes more aggressively

This is because compounding accelerates over time. The earlier you begin, the longer your investments can grow tax-advantaged within the IRA.

Who Should Consider an IRA?

An IRA is especially valuable if:

- You don’t have access to an employer-sponsored plan

- You are self-employed

- You want to supplement your existing 401(k) savings

Professional insight: Think of an IRA not just as a savings account, but as a long-term growth engine. The earlier you activate it, the more powerful it becomes.

2. You Don’t Need to Max Out Contributions to Make Progress

One of the most common misconceptions about IRAs is that you must contribute the full annual limit to make it worthwhile.

That’s simply not true.

Start Small, Stay Consistent

While $7,000 may feel like a large amount—especially for younger investors or those just beginning their financial journey—you are not required to contribute it all at once.

Instead, you can:

- Set up automatic weekly, biweekly, or monthly contributions

- Invest manageable amounts over time

- Build consistency without financial strain

For example:

- Contributing just $100–$300 per month can still lead to significant long-term growth

The Power of Habit Over Size

Consistency often matters more than contribution size.

Small, regular contributions:

- Reduce the psychological barrier to investing

- Help establish disciplined financial habits

- Allow you to benefit from dollar-cost averaging

Over time, these incremental contributions compound into meaningful wealth.

Avoiding Costly Mistakes

While contributing less than the maximum is perfectly fine, it’s important to:

- Avoid exceeding the annual contribution limit

- Excess contributions may trigger tax penalties each year until corrected

Professional insight: The key is not perfection—it’s participation. A steady, disciplined approach often outperforms sporadic large contributions.

3. Take Advantage of Valuable Tax Benefits

The defining feature of an IRA is its tax efficiency. There are two primary types—Traditional IRA and Roth IRA—each offering distinct advantages depending on your financial situation.

Traditional IRA: Immediate Tax Relief

A Traditional IRA allows you to potentially:

- Deduct contributions from your taxable income (depending on eligibility)

- Benefit from tax-deferred growth

This means:

- You may lower your tax bill today

- Your investments grow without being taxed annually

- Taxes are paid later when you withdraw funds in retirement

However, there are important considerations:

- Deductibility depends on your income level and whether you have access to a workplace retirement plan

- Required Minimum Distributions (RMDs) generally begin at age 73

- Early withdrawals (before age 59½) may incur a 10% penalty, unless exceptions apply

Roth IRA: Tax-Free Income in Retirement

A Roth IRA flips the tax model:

- Contributions are made with after-tax dollars (no immediate deduction)

- Investments grow tax-deferred

- Qualified withdrawals in retirement are completely tax-free

Additional benefits include:

- No required minimum distributions during your lifetime

- Greater flexibility in retirement income planning

- Ability to withdraw contributions (not earnings) at any time without tax or penalty

However:

- Roth IRAs are subject to income eligibility limits

- Not all investors qualify to contribute directly

Choosing Between Traditional and Roth

The decision often comes down to one key question:

Do you expect your tax rate to be higher now or in retirement?

- If you believe your current tax rate is lower, a Roth IRA may be advantageous

- If you want immediate tax savings, a Traditional IRA may be more suitable

You can also diversify by contributing to both (within total contribution limits), creating tax flexibility in retirement.

Professional insight: Tax diversification is a powerful but often overlooked strategy. Having both taxable and tax-free income sources can give you more control over your future tax liability.

Why Acting Now Matters

Timing is critical—not just in markets, but in tax planning.

With the 2025 IRA contribution deadline set for April 15, 2026, you still have an opportunity to:

- Reduce your taxable income (if eligible)

- Boost your retirement savings

- Capture another year of tax-advantaged growth

Delaying contributions means losing valuable time in the market—time that cannot be recovered.

Final Thoughts: Small Steps, Big Impact

An IRA is one of the most accessible and effective tools for building long-term financial security.

To recap, contributing now allows you to:

- Leverage compounding to grow your wealth over time

- Build consistency through manageable, automated contributions

- Optimize taxes with either immediate deductions or tax-free retirement income

The beauty of an IRA lies in its simplicity and flexibility. You don’t need to be a high-income investor or a market expert to benefit—you simply need to start.

Advisor’s closing perspective:

The most important investment decision is not choosing the perfect asset—it’s committing to the process. Start where you are, contribute what you can, and let time and discipline do the heavy lifting.

Your future self will thank you.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/3-powerful-reasons-to-contribute-to-an-ira-now-unlock-tax-advantages-and-accelerate-your-retirement-wealth.html