Market volatility is an inevitable part of investing. Whether driven by economic uncertainty, geopolitical events, or shifting interest rates, periods of market turbulence can test even the most disciplined investors. But volatility is not just a risk—it’s also an opportunity.

As a financial advisor, I often remind clients that what matters most is not reacting emotionally to short-term swings, but taking deliberate, strategic actions that strengthen your financial foundation and enhance long-term outcomes.

Below are five smart money moves you can make right now to build a stronger financial cushion, optimize your tax situation, and position your portfolio for future growth potential.

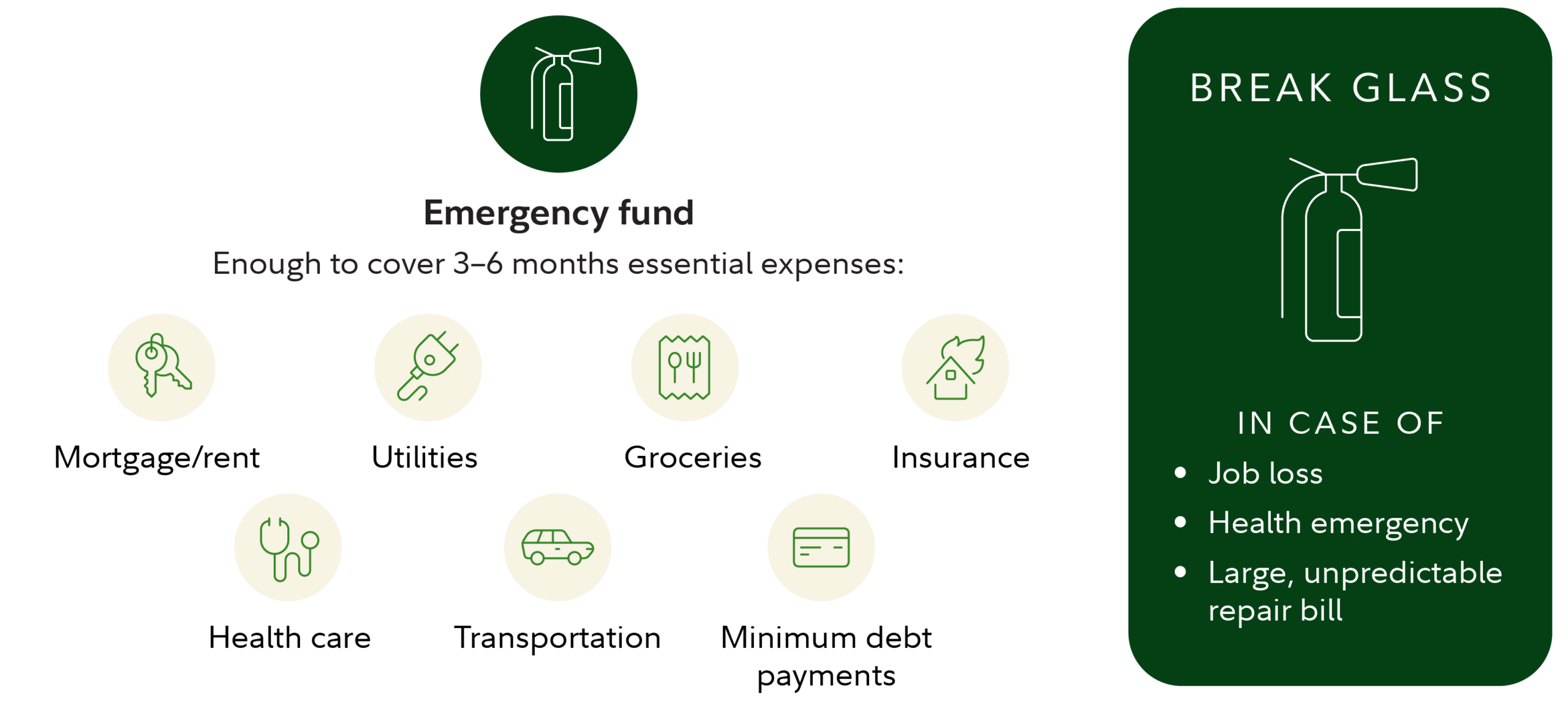

1. Strengthen Your Emergency Fund: Your First Line of Defense

Before focusing on returns, focus on resilience.

An emergency fund is the cornerstone of any sound financial plan. It provides liquidity during unexpected events—job loss, medical expenses, or sudden repairs—so you don’t have to sell investments at an inopportune time.

A practical approach is to:

- Start with a baseline goal of $1,000 in readily accessible cash

- Gradually build toward 3 to 6 months of essential living expenses

- Increase that cushion if:

- You are the sole income earner

- Your income is variable or uncertain

- You anticipate potential job changes

In volatile markets, this buffer becomes even more critical. It allows you to stay invested and avoid locking in losses simply to meet short-term cash needs.

Advisor insight: Think of your emergency fund as “portfolio insurance.” It may not generate returns, but it protects your long-term strategy.

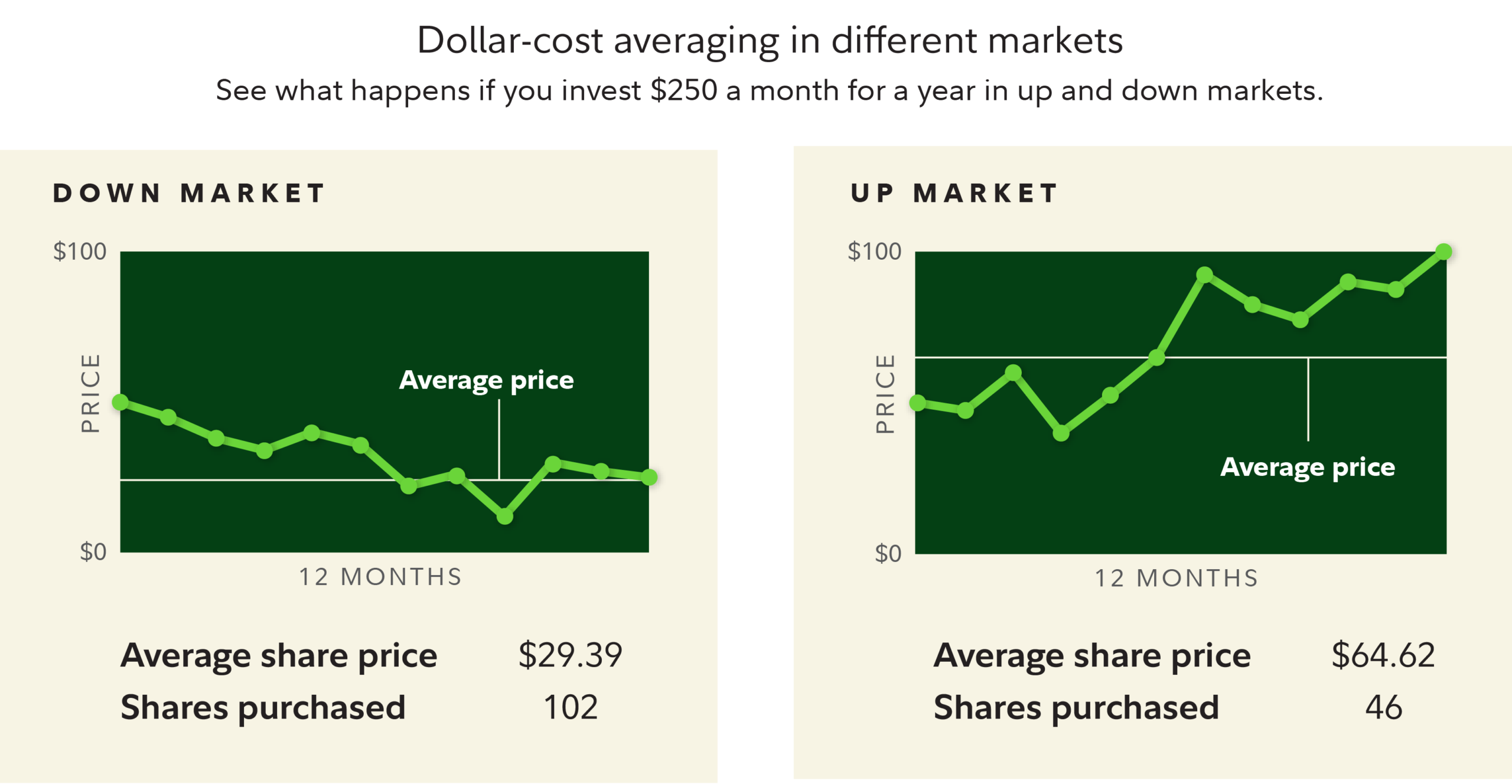

2. Automate Your Investing with Dollar-Cost Averaging

One of the biggest threats to investment success is emotional decision-making. Fear and greed often lead investors to buy high and sell low.

A simple yet powerful solution is dollar-cost averaging (DCA)—investing a fixed amount at regular intervals regardless of market conditions.

For example:

- Investing $250 per month into a mutual fund or ETF

- Continuing consistently through both rising and falling markets

This approach offers two key advantages:

- In declining markets, your fixed investment buys more shares at lower prices

- In rising markets, you benefit from continued participation and compounding

Over time, DCA helps smooth out the average cost of your investments and removes the need to “time the market”—a notoriously difficult task even for professionals.

Advisor insight: Automation creates discipline. Set up recurring investments through your brokerage or retirement account so your strategy runs in the background, regardless of market noise.

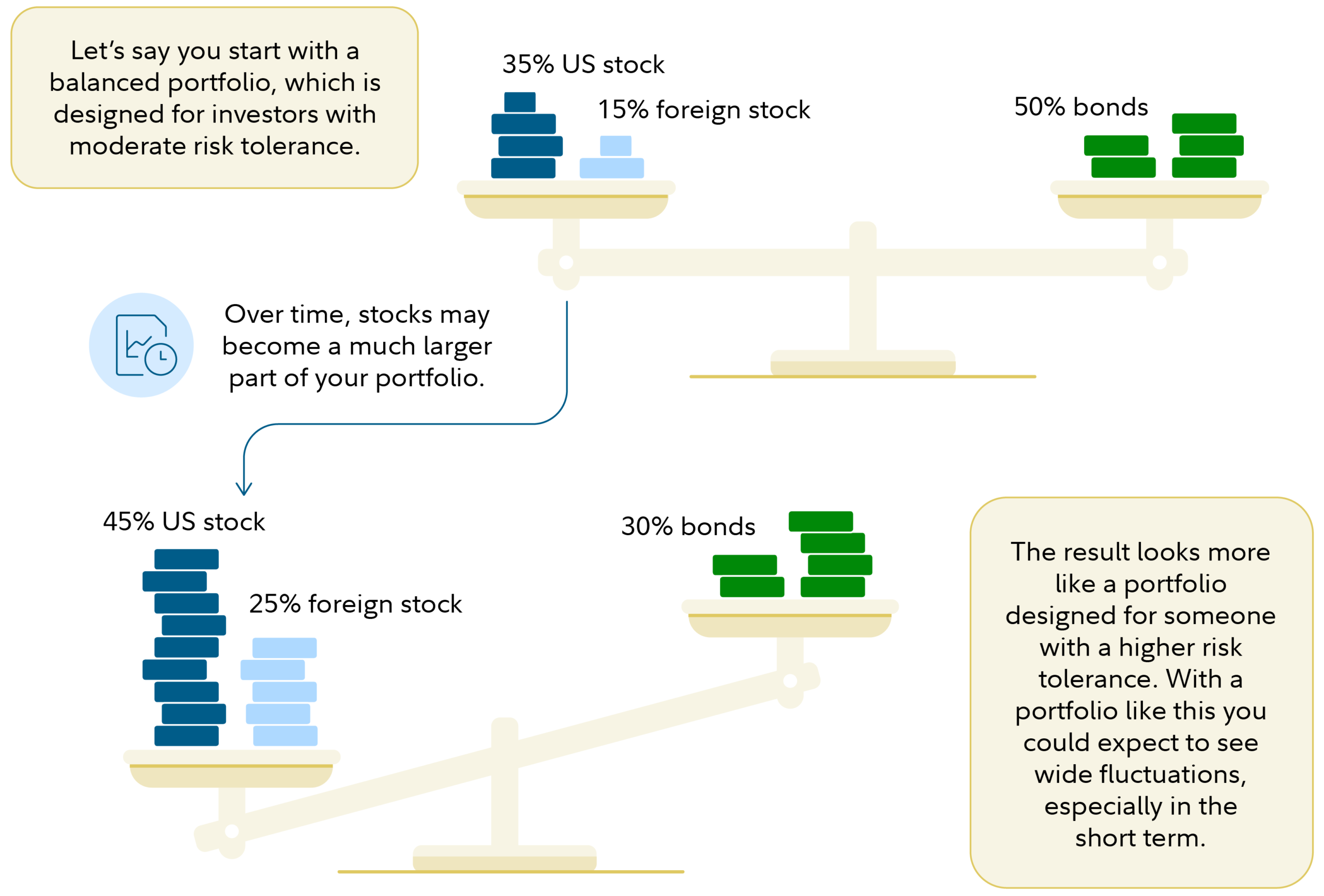

3. Rebalance Your Portfolio to Manage Risk

After extended market rallies, your portfolio may drift away from its original allocation.

For instance, the S&P 500 has delivered strong gains over the past several years. While that’s positive, it may also mean that equities now represent a larger portion of your portfolio than intended—exposing you to higher risk.

Rebalancing involves:

- Reducing overweight positions (e.g., stocks that have grown significantly)

- Adding to underweight assets (e.g., bonds or international exposure)

- Restoring your target asset allocation

Benefits of rebalancing include:

- Maintaining your intended risk level

- Enhancing diversification

- Systematically “selling high and buying low”

Advisor insight: Rebalancing is not about predicting the market—it’s about aligning your portfolio with your financial goals and risk tolerance. Consider reviewing your allocation at least once or twice a year.

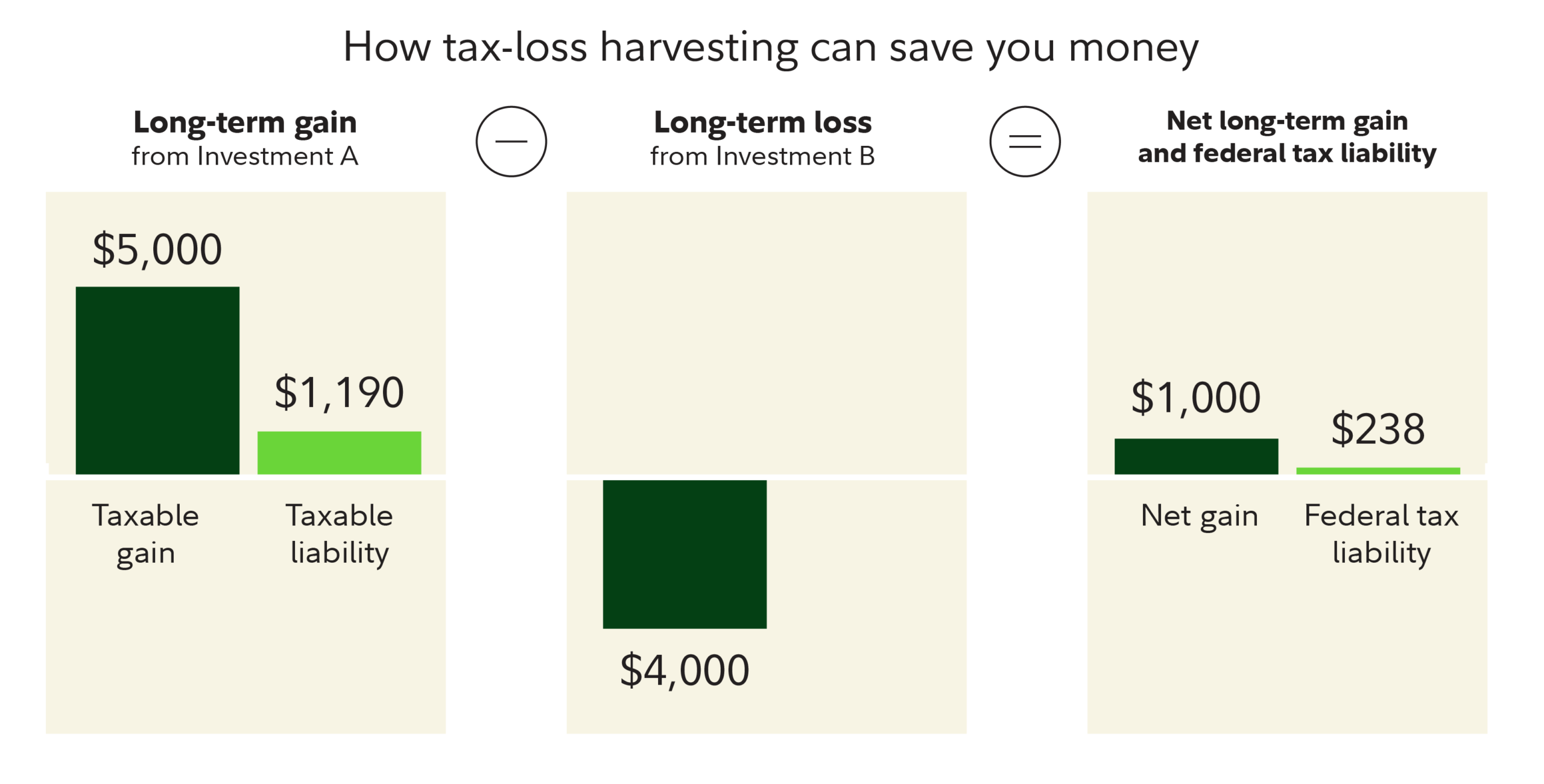

4. Use Tax-Loss Harvesting to Improve After-Tax Returns

Taxes can significantly impact your net investment returns. One effective strategy during volatile markets is tax-loss harvesting.

Here’s how it works:

- Sell investments that are currently below your purchase price (realizing a loss)

- Use those losses to offset realized capital gains

- If losses exceed gains, you can offset up to $3,000 of ordinary income annually

This can reduce your tax liability while allowing you to reinvest in similar (but not identical) assets to maintain market exposure.

However, there are important considerations:

- Be mindful of the Internal Revenue Service wash-sale rule, which disallows a loss if you repurchase the same or a “substantially identical” security within 30 days

- Ensure that tax strategies do not override your broader investment objectives

Advisor insight: Tax-loss harvesting is most valuable in taxable accounts and works best as part of an ongoing, systematic strategy—not a one-time move.

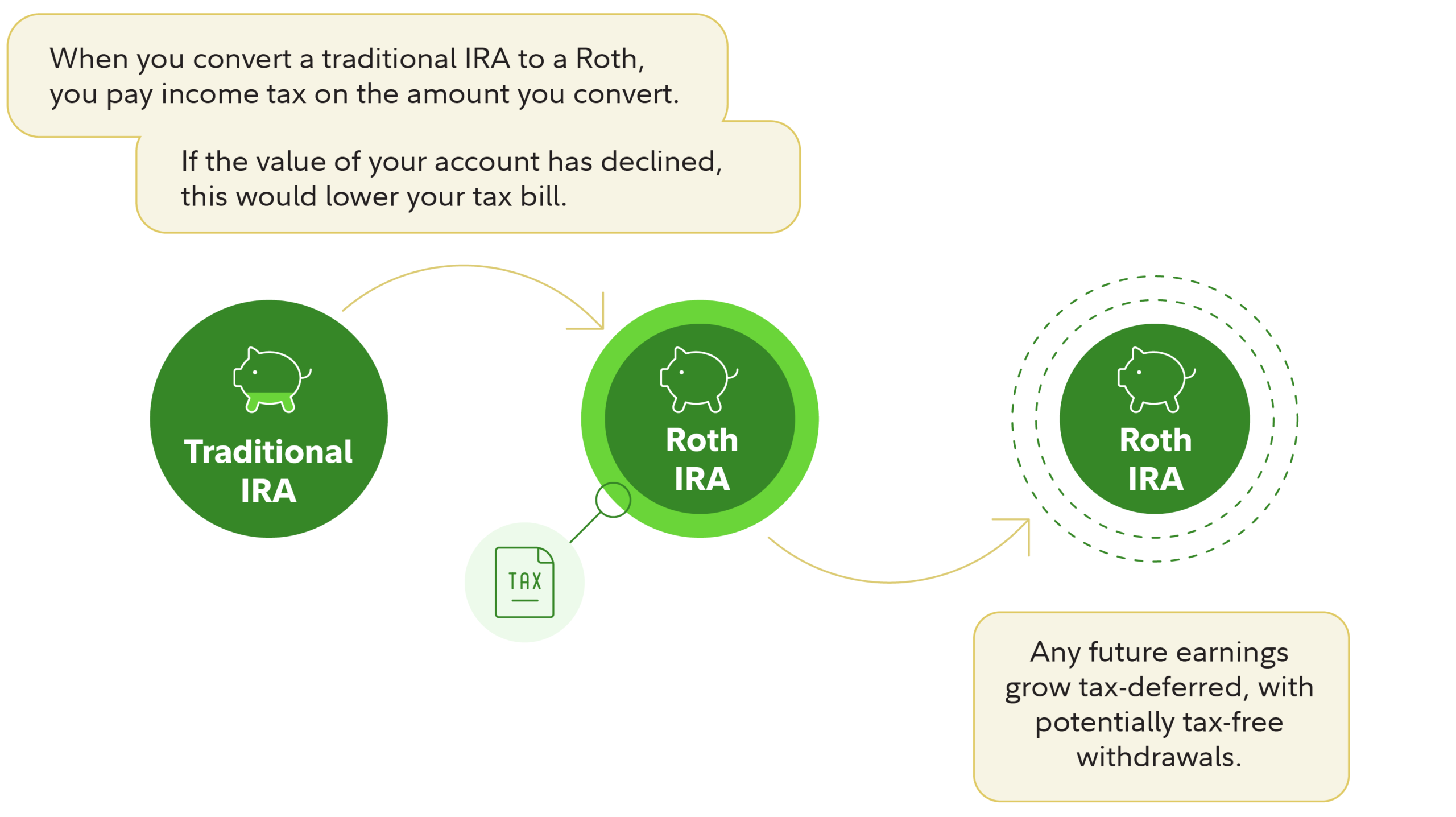

5. Consider a Roth Conversion During Market Declines

Market downturns can create unique tax planning opportunities—particularly for retirement accounts.

A Roth conversion involves transferring assets from a traditional IRA or 401(k) into a Roth IRA, paying taxes on the converted amount today in exchange for tax-free growth and withdrawals in the future.

Why consider this during a downturn?

- Your account value may be temporarily lower

- You pay taxes on a reduced valuation

- Future recovery and growth occur within the tax-free Roth structure

Additional advantages of Roth accounts:

- No required minimum distributions (RMDs) during your lifetime

- Greater flexibility in retirement income planning

- Potential tax diversification

Advisor insight: Roth conversions can be highly beneficial, but they require careful planning. Consider factors such as your current tax bracket, future income expectations, and available cash to pay the conversion taxes.

The Bottom Line: Stay Strategic, Not Reactive

Market volatility can feel unsettling—but it’s also a reminder of why having a disciplined financial plan is so important.

Instead of reacting emotionally, focus on what you can control:

- Strengthening your financial safety net

- Maintaining consistent investment habits

- Managing risk through rebalancing

- Optimizing taxes with thoughtful strategies

- Leveraging opportunities created by market declines

The most successful investors are not those who avoid volatility, but those who use it to their advantage.

If your plan is well-constructed and aligned with your goals, the best course of action is often to stay the course—while making targeted adjustments that improve your financial position over time.

Final Thought from an Advisor

In uncertain markets, clarity and discipline become your greatest assets.

By implementing these five smart money moves, you’re not just reacting to volatility—you’re building a more resilient, tax-efficient, and growth-oriented financial future.

And that’s what long-term investing is all about.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/5-smart-money-moves-now-how-to-build-financial-resilience-reduce-taxes-and-position-your-portfolio-for-long-term-growth.html