For an asset class with over 5,000 years of monetary history, gold is experiencing something unusual: a surge in modern investor attention. After an extraordinary rally—highlighted by a 65% gain in 2025 and prices briefly exceeding $5,000 per ounce—many investors are now asking a critical question:

Have we missed the opportunity, or are we still early in a long-term structural shift?

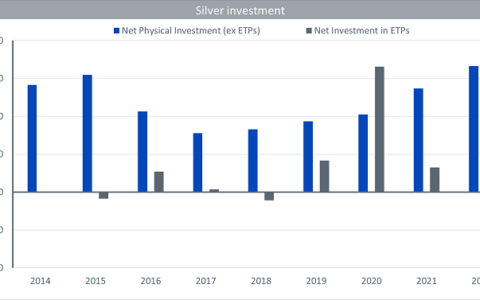

At the same time, silver has delivered even more dramatic gains, rising nearly 190% since early 2024. These moves have created both excitement and hesitation. Investors who lack exposure fear missing out, while others worry about buying at the top.

In this article, we’ll break down what’s driving the surge in precious metals, whether it’s too late to invest, and how investors should think about gold and silver in a modern portfolio.

The Big Picture: A Historic Rally with Deep Roots

Gold and silver are not rising in isolation—they are being propelled by a convergence of powerful macroeconomic forces.

Even after recent pullbacks, gold remains up more than 100% since early 2024, while silver has significantly outpaced it. Importantly, this rally is not purely speculative. It reflects structural changes in the global financial system, including:

- Central bank diversification away from the U.S. dollar

- Persistent inflation concerns

- Rising geopolitical instability

- Expanding fiscal deficits

This combination has created what some experts describe as a “new paradigm” for precious metals.

What’s Driving Gold and Silver Higher?

1. Central Banks Are Buying Gold Aggressively

One of the most important—and underappreciated—drivers is central bank demand.

Since 2022, global central banks have roughly doubled their annual gold purchases, from around 500 tons to over 1,000 tons. This demand now accounts for approximately 20% of total global gold consumption.

Why the shift?

- The freezing of Russian reserves highlighted geopolitical risks of holding dollar-based assets

- Emerging market central banks are diversifying reserves

- Gold is viewed as a neutral, globally accepted store of value

For example, China has reduced its U.S. Treasury holdings while significantly increasing its gold reserves.

Key takeaway: This is not short-term speculation—it’s a long-term structural reallocation.

2. Inflation, Debt, and Currency Concerns

Gold has historically acted as a hedge against inflation and currency debasement. While real interest rates have risen in recent years (which would normally pressure gold), prices have continued to climb.

Why?

- Massive government deficits are raising long-term concerns about currency stability

- The U.S. dollar has weakened over time despite short-term rallies

- Investors are seeking protection against erosion of purchasing power

Silver, while also a monetary metal, benefits additionally from industrial demand, particularly in:

- Solar panels

- Electronics

- Clean energy infrastructure

This dual demand profile helps explain why silver has outperformed gold during this cycle.

3. Geopolitics and De-Globalization

The global environment has become increasingly unstable:

- War in Eastern Europe

- Rising tensions in the Middle East

- Trade wars and tariffs

- Fragmentation of global supply chains

This has accelerated a broader trend of de-globalization, which often supports commodities, especially precious metals.

Gold thrives in uncertainty. Silver follows when commodity momentum broadens.

The Investor Dilemma: Buy Now or Wait?

After such a strong rally, investors face a classic problem:

- Buy now: Risk entering near a short-term peak

- Wait: Risk missing further upside

The reality is that timing precious metals is extremely difficult, even for professionals.

A Better Framework: Think Long-Term, Not Tactical

Instead of asking “Is now the perfect entry point?”, consider:

- Does gold/silver improve my portfolio diversification?

- Do I have exposure to assets that behave differently from stocks and bonds?

- Am I protected against inflation and geopolitical risk?

Historically, gold has performed well during market stress. For example, during the stock market correction in April 2025, gold prices rose—highlighting its role as a portfolio stabilizer.

How to Invest in Gold and Silver

If you decide to gain exposure, there are several approaches—each with different risk/reward profiles.

1. Bullion (Physical or ETFs)

- Tracks the spot price of gold or silver

- Can be accessed via ETFs (most common method)

- Lower volatility than mining stocks

- May include storage or management fees

Best for: Investors seeking direct exposure with simplicity

2. Gold Mining Stocks

- Highly sensitive to gold prices

- Historically move about 2x the price of gold

- Can deliver outsized returns in bull markets

However, they come with additional risks:

- Operational challenges

- Political risks (many mines are in emerging markets)

- Management quality

Example dynamic: When gold rose 65%, mining stocks surged 166%.

Best for: Experienced investors willing to take on higher volatility

3. Royalty & Streaming Companies

These companies:

- Finance mining projects

- Receive a percentage of production or revenue

Advantages:

- Lower operational risk than miners

- Strong cash flow profiles

Best for: Investors seeking a middle ground between bullion and miners

4. Diversified Commodity Funds

Instead of focusing only on precious metals, investors can allocate to broader commodity funds that include:

- Gold & silver

- Energy (oil, gas)

- Base metals (copper)

- Agriculture

This approach provides:

- Diversification within commodities

- Professional management

- Flexibility across market cycles

How Much Gold and Silver Should You Own?

This is one of the most important—and misunderstood—questions.

Even professional portfolio managers often allocate less than 1% to commodities in diversified portfolios, due to:

- High volatility

- Lack of income generation

- Cyclical nature

At the same time, most stock portfolios already have indirect exposure to commodities through sectors like energy and materials.

General Guidelines:

- Conservative investors: 0–5% allocation

- Moderate diversification: 5–10%

- Aggressive positioning: 10%+ (higher risk)

The key is balance—gold and silver should complement, not dominate, a portfolio.

Risks Investors Must Understand

Despite the strong narrative, precious metals are not risk-free.

Key Risks:

- Volatility: Prices can swing significantly

- No income: Unlike stocks or bonds, metals generate no cash flow

- Unpredictable cycles: Bull markets can last years—but also reverse sharply

As one portfolio manager noted, even after a “stupendous” year, it’s extremely difficult to predict how long the rally will continue.

So… Is It Too Late?

Short answer: No—but your mindset matters.

If you’re trying to chase quick gains, you may be late.

If you’re building a long-term diversified portfolio, you may still be early.

The forces supporting gold and silver—central bank demand, geopolitical shifts, inflation concerns—are not short-term trends. They are structural changes that could persist for years.

Final Take: Gold & Silver as Strategic Insurance

Gold and silver should not be viewed primarily as speculative trades.

Instead, think of them as:

- Portfolio insurance

- Inflation hedge

- Diversification tool

The goal is not to “beat the market” with gold—but to reduce overall portfolio risk while maintaining exposure to global uncertainty.

Bottom Line

- The recent rally in gold and silver is driven by deep structural forces

- It’s nearly impossible to time the perfect entry point

- Precious metals are best used for diversification—not speculation

- Allocation should be measured and aligned with your risk tolerance

For investors willing to think long-term, gold and silver may still have a meaningful role to play—not as a bet on price, but as a hedge against uncertainty in an increasingly complex world.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/gold-silver-at-record-highs-is-it-too-late-or-just-the-beginning-of-a-new-bull-cycle.html