Not every investor wants to spend evenings reading earnings reports, comparing stock charts, or adjusting a portfolio after every market move. Some people genuinely enjoy picking individual stocks and fine-tuning their investments. But many others simply do not have the time, interest, or confidence to manage their money on their own.

That does not make them bad investors. In fact, for many people, doing less can actually lead to better long-term results.

Modern “hands-off” investing options make it easier than ever to build a disciplined, diversified portfolio without managing every detail yourself. With the help of financial professionals, automated technology, managed accounts, and all-in-one funds, investors can stay focused on their long-term goals while reducing the temptation to make emotional decisions.

The goal is not to ignore your money. The goal is to invest smarter—with less daily effort.

What Is Hands-Off Investing?

Hands-off investing means delegating part or all of the portfolio management process to a professional advisor, a digital investing platform, or a fund that automatically adjusts over time.

Instead of personally choosing every stock, bond, ETF, or mutual fund, you rely on a structured investment solution to build, monitor, rebalance, and in some cases, tax-manage your portfolio.

This approach can be especially useful for investors who want to stay invested but do not want to constantly make decisions. A well-designed hands-off strategy can help maintain diversification, keep risk aligned with your goals, and reduce the urge to react emotionally during market volatility.

As Fidelity’s Jill Maher put it, delegating investment decisions is not about walking away from your financial goals. It is about choosing consistency over complexity. For investors who may not have the time, willingness, or skill to manage a portfolio themselves, a hands-off solution may give them a better chance of staying on track.

Hands-off investing is not only for beginners. It can also be a smart choice for experienced investors, busy professionals, families, retirement savers, and anyone who wants a disciplined long-term plan without having to manage every detail personally.

Why Investing With Less Work Can Be Smarter

A common misconception is that more activity means better investing. In reality, many investors hurt their returns by trading too often, chasing hot stocks, selling during downturns, or failing to rebalance their portfolios.

Hands-off investing can help solve several common problems.

First, it can help investors stay consistent. Markets go up and down, but a professionally managed or automated solution can keep the portfolio aligned with the original plan instead of reacting to fear or excitement.

Second, many hands-off strategies include automatic rebalancing. This means the portfolio is adjusted when market movements push it away from the target mix. For example, if stocks rise sharply and become too large a portion of the portfolio, the system may sell some stocks and buy more bonds to restore the intended balance.

Third, some managed solutions may offer tax-smart strategies, such as tax-loss harvesting, capital gains management, or tax-aware withdrawals. These are strategies many individual investors know about but may not execute consistently or correctly on their own.

Finally, hands-off investing reduces decision fatigue. Instead of constantly asking, “Should I buy now?” or “Should I sell?” investors can rely on a disciplined system and focus on the bigger picture.

Here are five practical ways to invest smarter with less work.

1. Use a Roboadvisor for Automated Portfolio Management

A roboadvisor is one of the most accessible hands-off investing tools available today. These digital platforms use technology to recommend, build, and manage a diversified portfolio based on your goals, time horizon, and risk tolerance.

Typically, a roboadvisor will invest your money across a mix of stocks, bonds, and cash equivalents. Once the portfolio is created, the platform monitors it and rebalances it when needed. This helps keep your asset allocation close to the original target.

For many investors, roboadvisors offer a good balance between professional portfolio management and low cost. They usually have lower account minimums and lower fees than traditional advisory services, making them appealing to younger investors, new investors, or anyone who wants a simple automated solution.

Some roboadvisor platforms also provide access to financial coaches, digital planning tools, budgeting guidance, retirement planning support, and tax-smart trading strategies. For example, Fidelity Go offers no advisory fee on balances under $25,000, while larger balances pay an annual fee that includes access to additional financial coaching and planning tools.

The main advantage of a roboadvisor is simplicity. You do not need to pick individual investments, monitor the market every day, or manually rebalance your account. The system handles much of the work in the background.

A roboadvisor may be a good fit if you want an affordable, automated investment solution and your financial situation is relatively straightforward.

2. Consider a Separately Managed Account for More Customization

A separately managed account, often called an SMA, is another hands-off investing option. With an SMA, you directly own the individual securities inside your account, but the portfolio is managed by investment professionals.

This is different from a mutual fund. When you buy a mutual fund, you own shares of a pooled investment vehicle. With an SMA, you may own the underlying stocks or bonds directly.

That direct ownership can offer several benefits. Investors may have more transparency into what they own, greater control over the portfolio, and more opportunities for tax-aware management. Some SMAs can also be customized around personal preferences, values, or investment restrictions.

For example, an investor may want to avoid certain industries, emphasize specific sectors, or use tax-loss harvesting to offset gains in a taxable account. A separately managed account may provide more flexibility than a traditional mutual fund.

Technology has also made SMAs more accessible. Digital managed account platforms can now build and oversee portfolios of individual stocks using strategies such as direct indexing or active management. Fidelity Managed FidFolios is one example of this type of approach.

The key appeal of an SMA is that it combines professional management with a higher level of personalization. It may be especially useful for investors with taxable accounts, concentrated positions, or specific preferences about how their money is invested.

An SMA may be a good fit if you want professional management but also want more control, transparency, and potential tax efficiency than a typical fund provides.

3. Hire a Financial Professional for Personalized Guidance

For investors with more complex financial lives, working with a financial advisor may provide the highest level of hands-off support.

A financial professional can do more than manage a portfolio. They can help you think through retirement planning, income strategies, tax-aware investing, estate considerations, major life events, college planning, and long-term financial goals.

This can be especially valuable when your financial situation involves multiple accounts, changing income, business ownership, inheritance, retirement transitions, or other major decisions.

A dedicated advisor can help build a diversified portfolio, monitor it over time, and adjust the strategy as your needs change. They can also help you avoid emotional mistakes during difficult markets. Sometimes the value of an advisor is not just in what they buy or sell, but in helping you stay disciplined when the market feels uncomfortable.

Many advisory services also use tax-smart techniques, diversified portfolios, and planning tools. Some services provide access to a team of financial planners once investors meet certain minimum investment levels.

Hiring a professional is usually more expensive than using a roboadvisor or an all-in-one fund, but the additional cost may be worthwhile for investors who need deeper planning and personalized advice.

A financial advisor may be a good fit if you want a human relationship, customized planning, and help with broader financial decisions beyond portfolio management.

4. Use Target-Allocation Funds for a One-Fund Portfolio

For investors who want simplicity, target-allocation funds can be an effective hands-off solution.

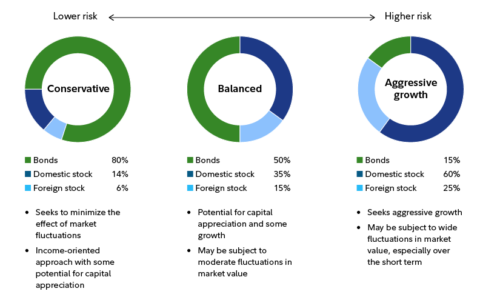

A target-allocation fund, also known as a target-risk fund or lifestyle fund, maintains a specific mix of stocks, bonds, and short-term investments based on a chosen risk level. For example, a moderate allocation fund might hold 60% stocks and 40% bonds.

The fund manager keeps the portfolio close to that target allocation by rebalancing over time. If stocks rise and become a larger share of the portfolio, the fund may sell some stocks and buy bonds. If stocks fall and become too small a portion, the fund may buy more stocks to return to the intended mix.

This built-in discipline can be hard for individual investors to maintain on their own. During strong markets, people often become too aggressive. During downturns, they may become too cautious. A target-allocation fund helps keep the strategy consistent.

These funds can range from conservative to aggressive. A conservative fund may hold a smaller percentage in stocks, while an aggressive growth fund may hold a much larger equity position.

The biggest advantage is convenience. With one fund, you can get a diversified portfolio that is professionally managed and automatically rebalanced.

A target-allocation fund may be a good fit if you want a simple, diversified portfolio with a stable risk level that does not automatically become more conservative over time.

5. Use Target-Date Funds for Retirement Investing

Target-date funds are especially popular in retirement accounts such as 401(k)s and IRAs.

A target-date fund is designed around an estimated retirement year. For example, someone planning to retire around 2055 might choose a 2055 target-date fund. The fund starts with a more growth-oriented allocation when retirement is far away and gradually becomes more conservative as the target date approaches.

This gradual shift is often called a glide path.

In the early years, target-date funds typically hold more stocks to pursue growth. As investors get closer to retirement, the fund usually increases exposure to bonds and other conservative investments to help reduce volatility and preserve capital.

This makes target-date funds appealing for investors who want a retirement portfolio that adjusts automatically over time. Instead of deciding when to reduce stock exposure or increase bonds, the fund handles those changes according to its built-in strategy.

Target-date funds are not perfect. Investors should still understand what they own, because different funds with the same target year can have different risk levels and asset allocations. But for many retirement savers, they offer a practical and easy-to-use solution.

A target-date fund may be a good fit if you are saving for retirement and want a single fund that becomes more conservative as you approach your retirement date.

The Benefits of Hands-Off Investing

The biggest benefit of hands-off investing is not just convenience. It is behavior management.

Many investors know what they should do in theory: diversify, rebalance, stay invested, think long term, and avoid emotional decisions. But in real life, that can be hard. Headlines, market volatility, social media, and short-term performance can all pressure investors into making poor choices.

Hands-off investing creates guardrails.

A managed or automated portfolio can help prevent common mistakes, such as selling during a market downturn or chasing a popular stock after it has already risen sharply. It can also help investors maintain a balanced portfolio instead of letting emotions drive decisions.

Another overlooked benefit is tax management. Some managed solutions can implement strategies such as tax-loss harvesting, capital gains management, and tax-smart withdrawals. These strategies may help improve after-tax results, especially in taxable accounts.

Consistency is another major advantage. A disciplined system can rebalance regularly, maintain diversification, and keep the portfolio aligned with the investor’s long-term plan.

Sometimes, stepping back is the smartest move.

How to Choose the Right Hands-Off Investing Option

The best hands-off investing choice depends on your financial goals, account size, complexity, and desired level of support.

Start by asking yourself a few honest questions:

Do I have the time to manage my investments properly?

Do I enjoy researching markets and making portfolio decisions?

Do I understand asset allocation, diversification, taxes, and rebalancing?

Can I stay calm when the market falls?

Do I want digital help, human advice, or a simple all-in-one fund?

If your answer is “no” to several of these questions, that does not mean you are lazy or incapable. It may simply mean that an automated or managed solution is a better fit.

A roboadvisor may work well if you want low-cost digital management. A separately managed account may be better if you want more customization and tax flexibility. A financial advisor may be the right choice if you need personalized planning. A target-allocation fund may work if you want a stable risk level in one fund. A target-date fund may be ideal if you want a retirement portfolio that adjusts over time.

That said, hands-off investing does not mean you should completely ignore your money. You should still review your accounts periodically, understand your general investment strategy, and revisit your plan when life changes.

A new job, marriage, children, a home purchase, retirement, or a major change in income can all be reasons to reassess your investment approach.

Final Thoughts: Smart Investing Does Not Have to Be Complicated

Investing smarter does not always mean working harder. In many cases, the smarter move is to build a system that keeps you disciplined, diversified, and focused on your long-term goals.

Hands-off investing can help reduce emotional decisions, automate rebalancing, add professional oversight, and potentially improve tax efficiency. Whether you choose a roboadvisor, a separately managed account, a financial advisor, a target-allocation fund, or a target-date fund, the key is to choose an approach that fits your life.

Some investors are well suited for self-directed investing. They enjoy the process, have the time to research, and are comfortable managing risk, taxes, and rebalancing. For those investors, doing it themselves can work well.

But for many people, delegating investment management is not a weakness. It is a practical decision.

Even financial professionals sometimes hire their own advisors because managing your own money can be emotionally different from managing someone else’s.

The most important step is to choose an investment strategy that matches your goals, abilities, and temperament—and then stick with it.

In the end, successful investing is not about doing the most work. It is about making thoughtful decisions, staying consistent, and giving your money the best chance to grow over time.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/5-smart-hands-off-investing-strategies-to-build-wealth-with-less-effort.html